The rise of stable QR pay 2026

The global payments infrastructure is undergoing a structural shift in 2026, moving away from speculative cryptocurrency trading toward fiat-backed utility. Stable QR pay has emerged as the primary vehicle for this transition, bridging the gap between traditional banking rails and decentralized finance. This convergence is not merely a technological upgrade; it is a redefinition of how cross-border commerce settles in real time.

Market data reflects this acceleration. Research from Juniper Research projects the QR code payments market to reach USD 19.81 billion in 2026, driven by a compound annual growth rate (CAGR) of approximately 19.1% [src-serp-4]. While early adoption focused on consumer convenience, the current growth engine is institutional. Merchants and financial institutions are leveraging stablecoins to reduce settlement costs and eliminate the friction of multi-currency reconciliation.

The technology behind stable QR pay 2026 relies on interoperable standards that allow a single QR code to trigger settlements in multiple currencies via stablecoin equivalents. This capability is particularly transformative for cross-border transactions, where traditional SWIFT networks often impose delays and opaque fees. By anchoring value to stable fiat currencies, these systems offer the speed of blockchain without the volatility that previously hindered enterprise adoption.

This integration is visible in emerging markets leading the charge. Vietnam, for instance, is actively testing stablecoin-to-QR payment rails to enhance financial inclusion and cross-border efficiency [src-serp-4]. As regulatory frameworks mature, the distinction between traditional digital payments and stablecoin-based QR systems is blurring, creating a unified global rail for value transfer.

Stable QR pay 2026 vs legacy rails

The migration to stable QR pay 2026 represents a structural shift from credit-based clearing to instant settlement. Traditional card networks and SWIFT wires rely on asynchronous messaging between multiple intermediaries, creating latency and opaque fee layers. Stablecoin infrastructure bypasses these bottlenecks by settling directly on the blockchain, offering a faster and more transparent alternative for cross-border commerce.

Fee structures and settlement speed

Card networks charge merchants interchange fees that typically range from 1.5% to 3.5%, plus cross-border surcharges. SWIFT transfers involve fixed wire fees and correspondent bank deductions, often taking 2-5 business days to clear. Stable QR pay 2026 reduces settlement times to seconds or minutes, with network fees often under 1%.

Volatility and regulatory compliance

While stablecoins are pegged to fiat assets, they still carry minor de-pegging risks compared to the guaranteed settlement of traditional banking rails. However, the transparency of on-chain ledgers provides superior auditability for compliance teams. As 2026 payment trends reshape Latin American and global commerce, the operational efficiency of stable QR systems is driving adoption despite these residual volatility considerations [src-serp-7].

Merchant adoption in high-growth regions

Merchant adoption of stable QR pay 2026 is accelerating in Southeast Asia and Latin America, driven by the urgent need to reduce remittance friction and bypass legacy banking infrastructure. In these markets, the technology is not merely a convenience but a critical utility for financial inclusion and cross-border efficiency.

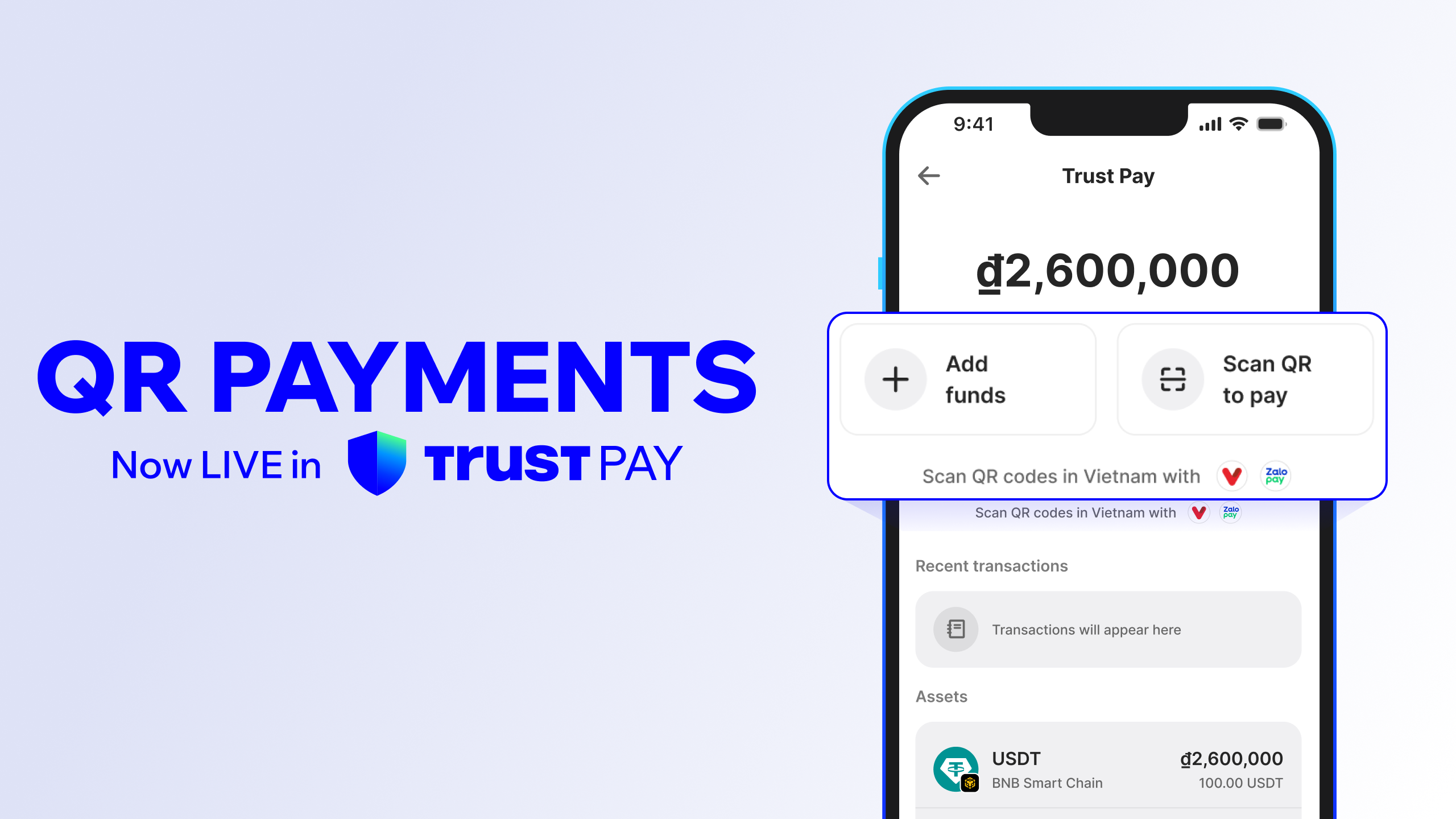

Vietnam tests the global rail

Vietnam is emerging as a primary testing ground for cross-border stablecoin integration. The market is projected to reach USD 19.81 billion by 2026, expanding at a CAGR of approximately 19.1% as merchants integrate QR codes that settle directly in stable assets rather than volatile local currencies [[src-serp-4]]. This shift allows remittance recipients to receive funds instantly without the traditional multi-day settlement delays.

The infrastructure supports this growth by treating QR codes as a universal settlement layer. Merchants accept the scan, and the backend network handles the stablecoin conversion and settlement, effectively turning the QR code into a borderless payment terminal.

Latin America’s transaction shift

In Latin America, the adoption of stable QR pay 2026 is reshaping how businesses handle high-volume, low-margin transactions. By 2026, stablecoins are expected to account for 18% to 22% of the cross-border payment volume in the region [[src-serp-7]]. This shift is driven by hyperinflationary pressures in countries like Argentina and Venezuela, where merchants use stable QR payments to preserve value between sales.

The QR standard provides a low-cost entry point for small merchants who cannot afford expensive POS hardware. By scanning a single QR code, businesses can accept payments in USDT or USDC, instantly settling in a stable asset that protects their margins from local currency devaluation.

Technical requirements for POS integration

Accepting stable QR pay 2026 demands that merchant hardware and software handle complex cryptographic verification without introducing latency. The core challenge lies in bridging traditional point-of-sale (POS) architectures with blockchain-based settlement layers. Modern POS systems must support dynamic QR generation and real-time validation of tokenized assets, ensuring that the transaction is recorded on the distributed ledger before the receipt is printed. This dual-layer verification prevents double-spending and ensures that the fiat equivalent is settled instantly.

Compatibility extends beyond the terminal to the backend payment gateway. Merchants using legacy systems often face integration friction because older APIs were designed for batch processing rather than real-time crypto-to-fiat conversion. To accept stable QR pay 2026, the POS middleware must interpret the QR data payload, which includes wallet addresses, asset types, and transaction hashes. This requires a robust API layer that can communicate with multiple stablecoin networks—such as USDC on Ethereum or USDT on Tron—simultaneously.

Security protocols must also evolve to meet new standards. The QR code itself is merely the trigger; the critical infrastructure is the wallet integration that processes the signature. Merchants need hardware security modules (HSMs) or cloud-based key management systems to securely store the merchant’s receiving addresses. Without these protections, the risk of address substitution attacks increases significantly. The system must also handle network congestion by automatically switching to alternative stablecoin routes if the primary network experiences high gas fees, ensuring the customer experience remains seamless.

Compliance and provider dependency

Stable QR pay 2026 operates within a stringent regulatory framework that demands rigorous adherence to anti-money laundering (AML) and know-your-customer (KYC) protocols. Merchants and payment processors must navigate a fragmented landscape where compliance standards vary by jurisdiction, creating significant operational overhead for cross-border transactions. Failure to maintain robust compliance infrastructure can result in frozen funds or permanent account bans, making regulatory alignment a prerequisite for market participation rather than an optional feature.

The infrastructure supporting these payments remains vulnerable to provider discontinuation, a risk recently highlighted by Trust Wallet. The platform announced that its QR payments feature would be temporarily discontinued on March 31, 2026, due to changes in its underlying payment provider. This move serves as a cautionary tale for merchants who have built their revenue streams on specific third-party integrations without securing fallback options.

Reliance on a single provider creates a single point of failure. When a major wallet or gateway alters its terms or ceases operations, merchants must rapidly migrate to alternative solutions, often during periods of high transaction volume. This dependency underscores the need for diversified payment routing and clear contractual safeguards. As the stablecoin payment ecosystem matures, regulatory clarity will likely shift from reactive enforcement to proactive licensing, further raising the barrier to entry for non-compliant actors.

No comments yet. Be the first to share your thoughts!