Why stable QR pay matters now

Small businesses are facing a squeeze from two sides. On one side, traditional payment processing fees continue to climb, eating into already thin margins. On the other, handling physical cash introduces security risks and operational friction that many merchants can no longer afford. Stable QR pay offers a direct path to bypass these bottlenecks by combining the speed of digital transactions with the price stability of fiat-pegged assets.

The economics of traditional card processing are becoming increasingly difficult for low-volume merchants. Standard credit card networks typically charge around 2.9% + $0.30 per transaction. For a $5 coffee sale, that fee represents nearly 9% of the revenue. In contrast, stablecoin transactions on efficient networks often cost fractions of a cent, regardless of the transaction size. This disparity allows small businesses to retain more of their earnings, turning micro-transactions from margin-killers into profitable opportunities.

Beyond fees, the risk profile of cash handling remains a significant burden. Cash requires secure storage, frequent bank deposits, and is vulnerable to theft and counterfeiting. Stable QR payments digitize the entire flow, reducing the need for physical currency on the premises. By adopting stable QR pay, merchants can streamline their operations while benefiting from the transparency and speed of blockchain settlement.

The shift isn't just about cost; it's about accessibility and speed. QR codes are universally understood and require no specialized hardware beyond a smartphone. This lowers the barrier to entry for merchants who might otherwise struggle with expensive point-of-sale terminals. As stablecoin infrastructure matures, the combination of low fees and ease of use positions stable QR pay as a practical alternative to cash and traditional card networks.

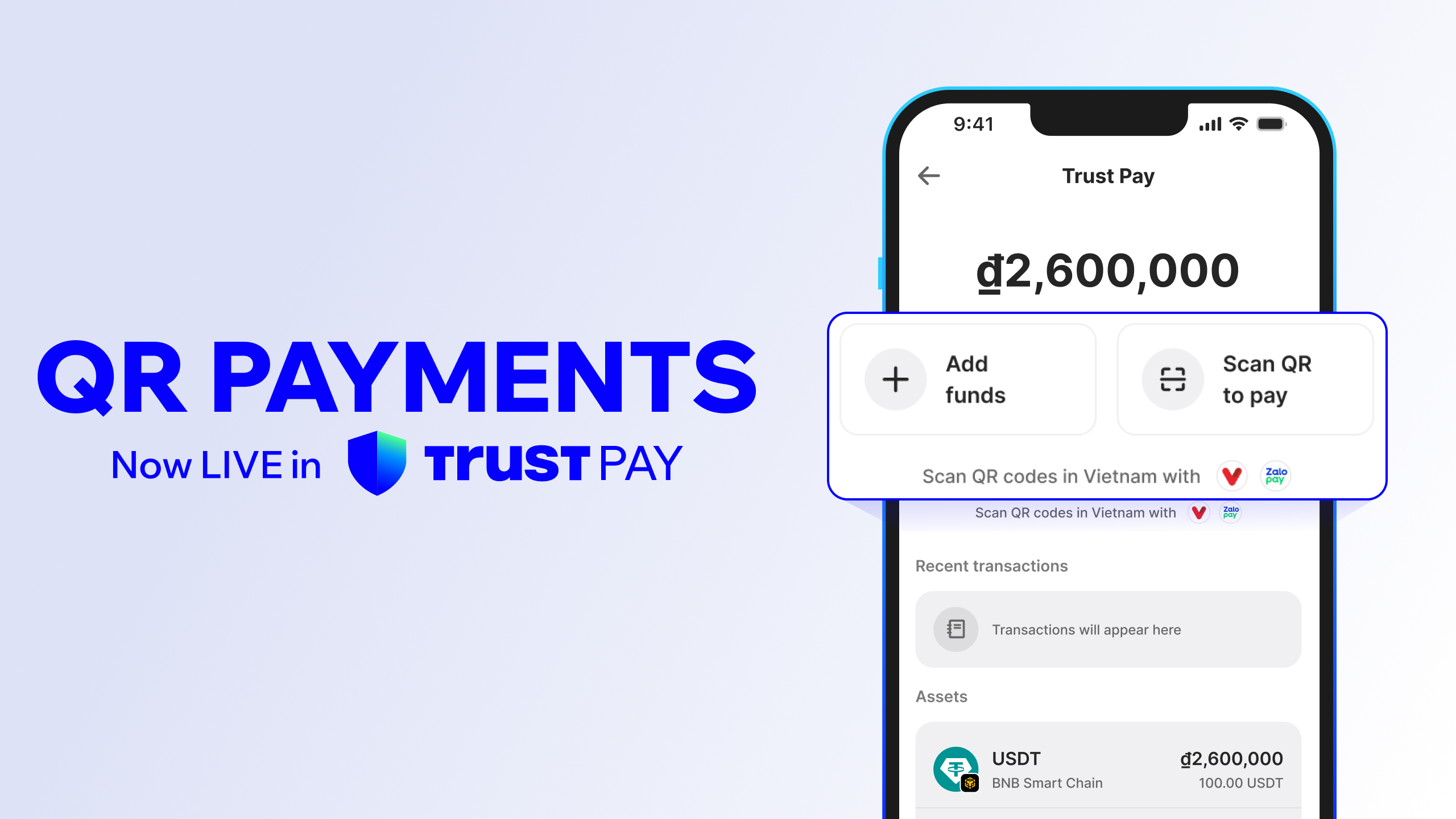

How stable QR pay works for merchants

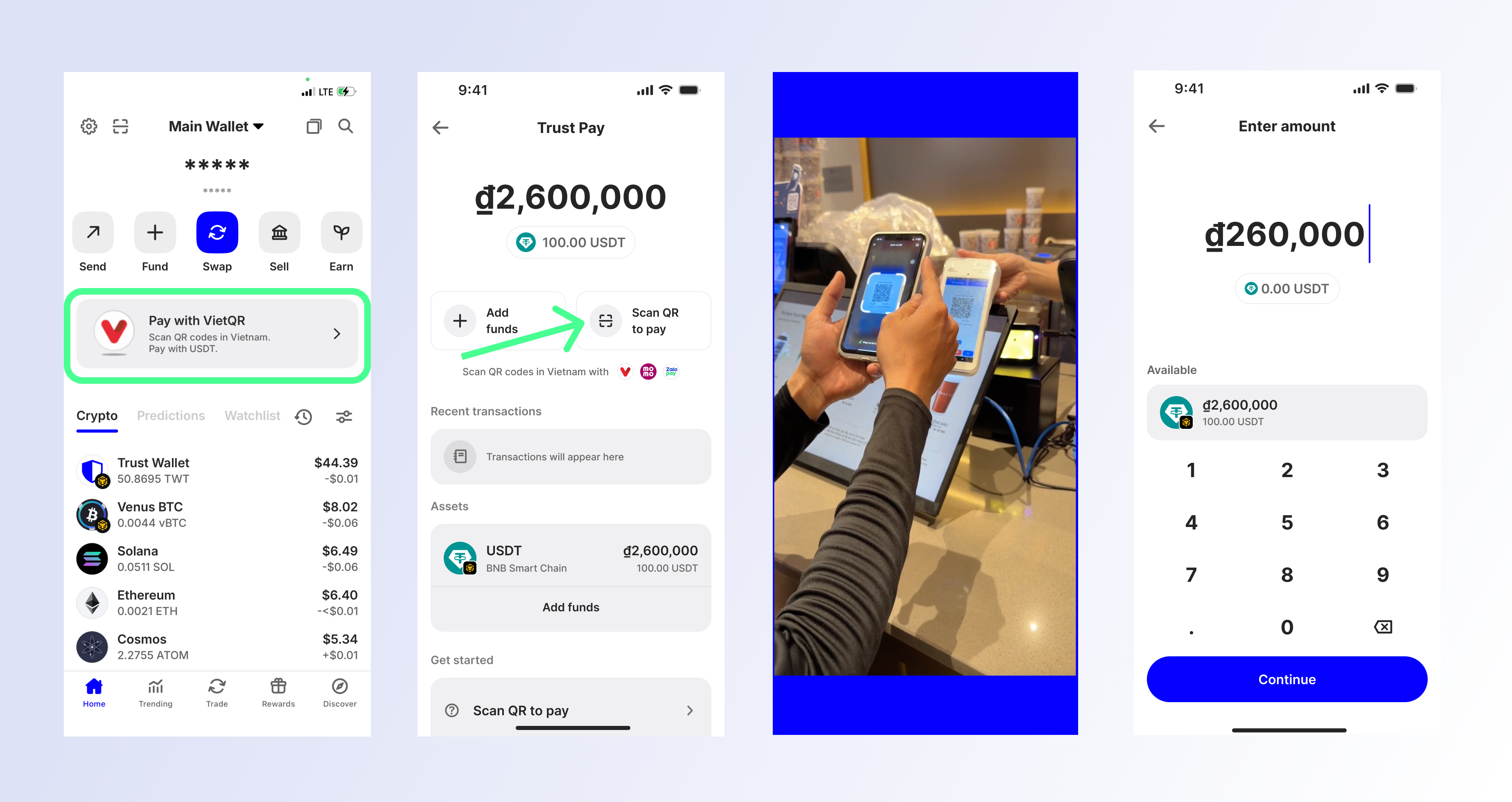

The technical flow of stable QR pay is designed to remove the lag and friction of traditional card processing. When a customer scans a merchant's QR code, the transaction initiates a blockchain transfer of a stablecoin, such as USDT or USDC. This step is immediate, typically settling in seconds rather than the days often required for bank clearing. For the merchant, the complexity lies in the backend conversion, ensuring they receive local currency without holding volatile digital assets.

This streamlined process relies on the reliability of stablecoin pegs. Merchants can trust that the value they receive is consistent with the price displayed to the customer. The following chart demonstrates the price stability of major stablecoins over the last 30 days, confirming their suitability for everyday retail transactions.

Top stable QR pay providers in 2026

The stable QR pay landscape in 2026 is defined by three distinct approaches to bridging crypto and cash. Trust Wallet prioritizes self-custody, allowing users to hold funds while merchants receive local currency. RedotPay focuses on debit card integration, converting stablecoins to fiat at the point of sale for everyday spending. Moreta targets cross-border efficiency, enabling travelers to pay foreign merchants instantly without currency exchange delays.

Each platform serves a different user need. Trust Wallet appeals to those who want full control over their assets. RedotPay suits users who prefer the convenience of a traditional card linked to crypto. Moreta is ideal for international transactions where speed and low fees matter most.

Comparison of leading platforms

The table below compares the core features of these providers. Fees, supported chains, and settlement times vary significantly. Choose the platform that aligns with your primary use case.

| Provider | Fees | Supported Chains | Settlement |

|---|---|---|---|

| Trust Wallet | Variable by network | Multi-chain | Instant (merchant) |

| RedotPay | Low transaction fee | Ethereum, BSC | Instant (card) |

| Moreta | Competitive FX rate | Multi-chain | Real-time (cross-border) |

Trust Wallet

Trust Wallet integrates QR payments directly into its self-custodial wallet. Users scan a merchant’s QR code to initiate a payment. The merchant receives local currency instantly, while the user retains control of their private keys. This model appeals to privacy-conscious users who want to spend stablecoins without surrendering custody. The platform supports multiple chains, reducing network dependency.

RedotPay

RedotPay simplifies stablecoin spending by linking crypto to a physical debit card. Users scan a QR code at merchants accepting VietQR or other local payment networks. The transaction converts stablecoins to fiat in real time. This approach removes the need for users to manage complex wallet interactions. It is particularly useful for everyday purchases where simplicity is key.

Moreta

Moreta focuses on cross-border payments for travelers. Users can scan a QR code to pay merchants abroad in local currency. The platform handles currency conversion and settlement in real time, eliminating the need for pre-travel currency exchange. This is especially valuable for international business or tourism, where speed and transparency matter.

Choosing the right provider

Select a provider based on your primary need. Use Trust Wallet for self-custody and multi-chain flexibility. Choose RedotPay for seamless everyday spending via a debit card. Opt for Moreta for efficient cross-border transactions. Each platform offers a distinct advantage in the stable QR pay ecosystem.

Setting up stable QR pay at your counter

Accepting stablecoin payments via QR codes requires minimal hardware and a focus on security. The goal is to replace cash handling with a digital flow that settles instantly in a stable asset like USDC. This section walks through the practical steps to get your counter ready.

Not all payment gateways support crypto. Look for providers that explicitly list stablecoin acceptance (USDC, USDT) and offer fiat settlement options. This ensures you get paid in dollars without holding volatile crypto assets. Check if the processor handles the technical bridging between the customer’s wallet and your bank account.

For fixed-price items (like a $5 coffee), a static QR code linked to your merchant wallet address works well. For variable amounts, use a dynamic QR code generated by your payment processor. Dynamic codes update the exact amount and order details in real-time, reducing errors and ensuring the customer pays the correct sum.

Stablecoin transactions are irreversible. Once the customer scans and confirms, the payment is instant. Do not release goods or services until the transaction appears in your merchant dashboard or wallet with the required number of confirmations. Most stablecoin networks settle in seconds, but a single confirmation is often sufficient for low-value retail transactions.

Your payment processor should automatically convert the stablecoin into fiat currency (USD, EUR, etc.) and deposit it into your business bank account. This step removes exchange rate risk. Review your daily settlement reports to ensure the amounts match your sales records. This bridges the gap between crypto innovation and traditional accounting.

No comments yet. Be the first to share your thoughts!