Why stable QR pay 2026 matters now

The shift from traditional card rails to stablecoin QR payments is no longer a theoretical experiment; it is an operational necessity for merchants who cannot afford delayed cash flow. Traditional settlement cycles often hold funds for days, creating liquidity gaps that strain small businesses. Stable QR pay 2026 resolves this by offering instant settlement, allowing merchants to access their revenue immediately after a transaction is completed.

This immediacy changes the fundamental economics of accepting payments. Instead of waiting 24 to 72 hours for card networks to clear, merchants see funds in their digital wallets in seconds. For offline retailers operating on thin margins, this speed reduces the need for working capital loans and simplifies daily reconciliation. The technology moves beyond mere convenience to become a critical infrastructure upgrade for cash flow management.

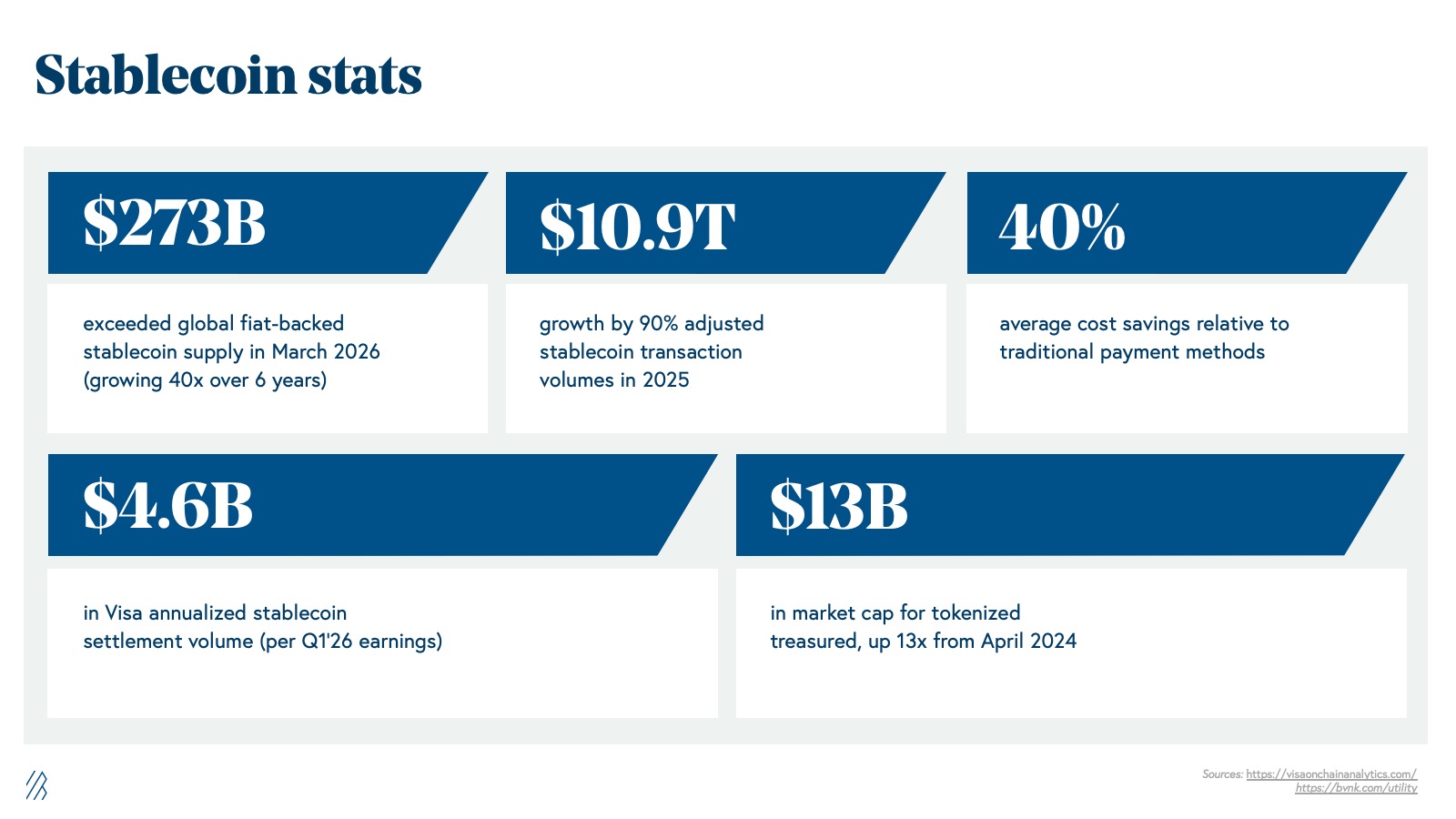

Market data supports this rapid adoption. Juniper Research projects that QR code payments will grow by 50% globally from $5.4 trillion in 2025 to exceed $8 trillion by 2029. This surge is not just about volume; it marks a critical inflection point where stablecoin integration becomes the dominant method for cross-border and domestic QR transactions. The infrastructure is ready, and the financial incentive for merchants to switch is now undeniable.

Instant settlement vs. traditional card rails

The difference between instant stablecoin settlement and traditional card processing is not just about speed; it is a fundamental shift in liquidity management. Traditional card rails operate on a delayed settlement cycle, typically T+1 or T+2, meaning merchants wait days to access their revenue. In contrast, stable QR payments offer T+0 settlement, delivering funds to the merchant’s wallet within seconds of the transaction.

This delay in traditional systems ties up working capital. For small merchants and offline retailers, cash flow is the lifeblood of daily operations. Waiting 48 hours for funds to clear creates friction, forcing businesses to rely on credit lines or reserves to cover immediate expenses. Instant settlement removes this bottleneck, allowing merchants to reinvest revenue immediately into inventory or staff.

Beyond timing, the fee structures diverge significantly. Traditional card processors charge interchange fees, assessment fees, and acquiring costs that often total between 2.9% and 3.5% per transaction. Stable QR payments, leveraging blockchain infrastructure, bypass these intermediaries. The result is a flat, predictable fee structure that is typically a fraction of traditional processing costs, preserving margin for the merchant.

The table below outlines the core operational differences between the two systems.

| Feature | Stable QR Pay | Traditional Card |

|---|---|---|

| Settlement Time | T+0 (Seconds) | T+1 to T+2 (Days) |

| Average Fee | 0.5% - 1.0% | 2.9% - 3.5% |

| Cross-Border | Native (24/7) | High FX Fees + Delays |

| Chargeback Risk | Irreversible | High (1-2% of volume) |

For merchants operating in high-volume, low-margin environments, these differences compound. The combination of immediate liquidity and lower fees directly improves net revenue. As the QR code-based payment market expands, driven by standards like X9.150, the infrastructure gap between instant crypto-settled payments and legacy banking rails continues to widen.

The X9.150 standard and global interoperability

The shift toward stable QR pay 2026 relies on a single technical breakthrough: the ANSI X9.150 standard. Previously, QR codes were simple pointers to payment pages, offering no way to verify the transaction details before scanning. X9.150 changes this by embedding structured data directly into the code, allowing merchants and banks to read the payer, payee, amount, and currency before the transaction is finalized. This provability is the foundation for instant settlement and offline resilience.

For offline merchants, this standard is a lifeline. When connectivity fails, the QR code contains all necessary instructions to queue the transaction locally. Once the device reconnects, the structured data ensures the payment clears without ambiguity or duplicate charges. This capability transforms QR codes from static links into dynamic, self-contained financial instruments that work regardless of network stability.

Global interoperability is equally critical. X9.150 is designed to align with ISO 18013-5, the standard for digital driver’s licenses and IDs, creating a unified framework for identity and payments. This alignment allows cross-border transactions to settle instantly using stablecoins, bypassing the delays and fees of traditional correspondent banking. As Vietnam and other markets test these rails, the standard is becoming the backbone of a borderless digital economy.

Stablecoin Stability and Market Growth

Merchants adopting stable QR payments need assurance that their settlement currency won't fluctuate wildly. The core advantage of using stablecoins like USDT or USDC for QR transactions is their pegged value, which effectively removes the volatility risk associated with other cryptocurrencies. This stability is critical for offline merchants who rely on predictable daily revenue to manage inventory and payroll.

To visualize this reliability, you can view the live price and historical performance of USDT against the US dollar below. The chart demonstrates how tightly the asset tracks the dollar, even during broader crypto market turbulence, ensuring that a $10 QR payment settles as $10 in value.

This stability supports a rapidly expanding market. QR code payments are projected to exceed $8 trillion globally by 2029, with the sector growing at a compound annual growth rate of roughly 19% through 2026. As the infrastructure matures, the integration of stablecoin settlements into these QR rails offers merchants a bridge between traditional fiat predictability and blockchain efficiency.

Choosing the right stable QR pay provider

Selecting a stable QR pay provider requires balancing three factors: fee structures, supported blockchain networks, and adherence to the new X9.150 standard. A provider that offers low fees but lacks compliance with emerging regulatory frameworks poses a higher long-term risk than a slightly more expensive, fully compliant option.

Compare fee structures and settlement times

Merchant processing fees typically range from 0.5% to 2% per transaction, depending on the provider and the underlying blockchain. Look for providers that offer flat-rate fees for high-volume merchants or zero fees for specific stablecoin pairs. Settlement speed is equally critical; some providers settle on-chain immediately, while others batch transactions for cost efficiency. For offline merchants, instant settlement ensures cash flow continuity without the lag of traditional banking rails.

Verify supported chains and X9.150 compliance

Not all stable QR pay providers support the same blockchain networks. Ensure your provider supports the stablecoins your customers prefer, such as USDC or USDT, and the specific chains that offer the best transaction speeds and lowest costs. More importantly, verify that the provider adheres to the X9.150 standard, which governs the secure transmission of payment data over QR codes. This standard is becoming a de facto requirement for interoperability and security in the stablecoin payment space.

Check for regulatory compliance and support

Finally, prioritize providers that operate within the regulatory frameworks of your target markets. Compliance with anti-money laundering (AML) and know-your-customer (KYC) regulations is non-negotiable for long-term viability. Additionally, consider the quality of customer support and the availability of technical documentation. A provider with robust support can help you navigate integration challenges and resolve issues quickly, minimizing downtime for your business.

Frequently asked questions about stable QR pay 2026

Is stablecoin QR pay volatile for merchants?

No. Stablecoins are pegged to fiat currencies like the US dollar, so their value remains steady during the transaction. This eliminates the price swings seen with Bitcoin or Ethereum. Merchants receive the exact dollar amount owed, protecting margins from market turbulence.

How fast is settlement compared to credit cards?

Settlement is near-instant, often arriving in your wallet within seconds rather than days. Credit card networks typically take two to three business days to clear funds. This rapid liquidity helps offline merchants manage cash flow without waiting for batch processing.

What if the customer has no internet connection?

The system works offline by storing transaction data locally and syncing once connectivity returns. The merchant scans the customer’s QR code, and the blockchain records the transfer in the background. This ensures payments go through even in basements or rural areas with poor signal.

Is stablecoin QR pay legal in my region?

Regulation varies by jurisdiction, but many regions are updating frameworks to accommodate digital assets. Check with your local financial authority or payment processor for specific compliance rules. The X9.150 standard, introduced in early 2026, aims to create a unified regulatory baseline for blockchain payments.

No comments yet. Be the first to share your thoughts!