The shift to stablecoin QR rails

The global payments infrastructure is undergoing a structural shift. QR code payments are no longer a niche alternative; they are becoming a primary settlement rail. Juniper Research projects the global value of QR payments will grow by 50% from $5.4 trillion in 2025 to exceed $8 trillion by 2029 [[src-serp-1]]. This expansion is driven by the need for lower-cost, cross-border compatible settlement layers that traditional card networks struggle to provide efficiently.

Stablecoin QR settlements represent the convergence of this established QR infrastructure with the utility of digital dollar assets. For merchants, the appeal lies in the cost-benefit analysis. Traditional card processing fees typically range from 1.5% to 3.5%, plus cross-border FX spreads. Stablecoin settlements on efficient chains can reduce these costs to fractions of a cent, while maintaining the familiarity of a QR-based checkout experience for consumers. This cost advantage is particularly significant for small businesses operating in high-volume, low-margin environments.

However, the transition is not without friction. Deloitte notes that while QR payments offer speed and accessibility, they can introduce checkout friction compared to NFC tap-to-pay methods [[src-serp-1]]. The security model of static QR codes requires robust verification to prevent man-in-the-middle attacks. The market is currently testing hybrid models where dynamic QR codes are generated per transaction, balancing the ease of use with the security requirements of financial-grade settlements.

The adoption of stablecoin QR rails is less about replacing existing payment methods entirely and more about creating a parallel, efficient settlement layer. As regulatory frameworks clarify and merchant acquiring systems integrate native stablecoin support, the economic incentive for adopting this technology will likely outweigh the implementation costs. The next phase of growth will depend on how seamlessly these systems integrate into existing point-of-sale hardware.

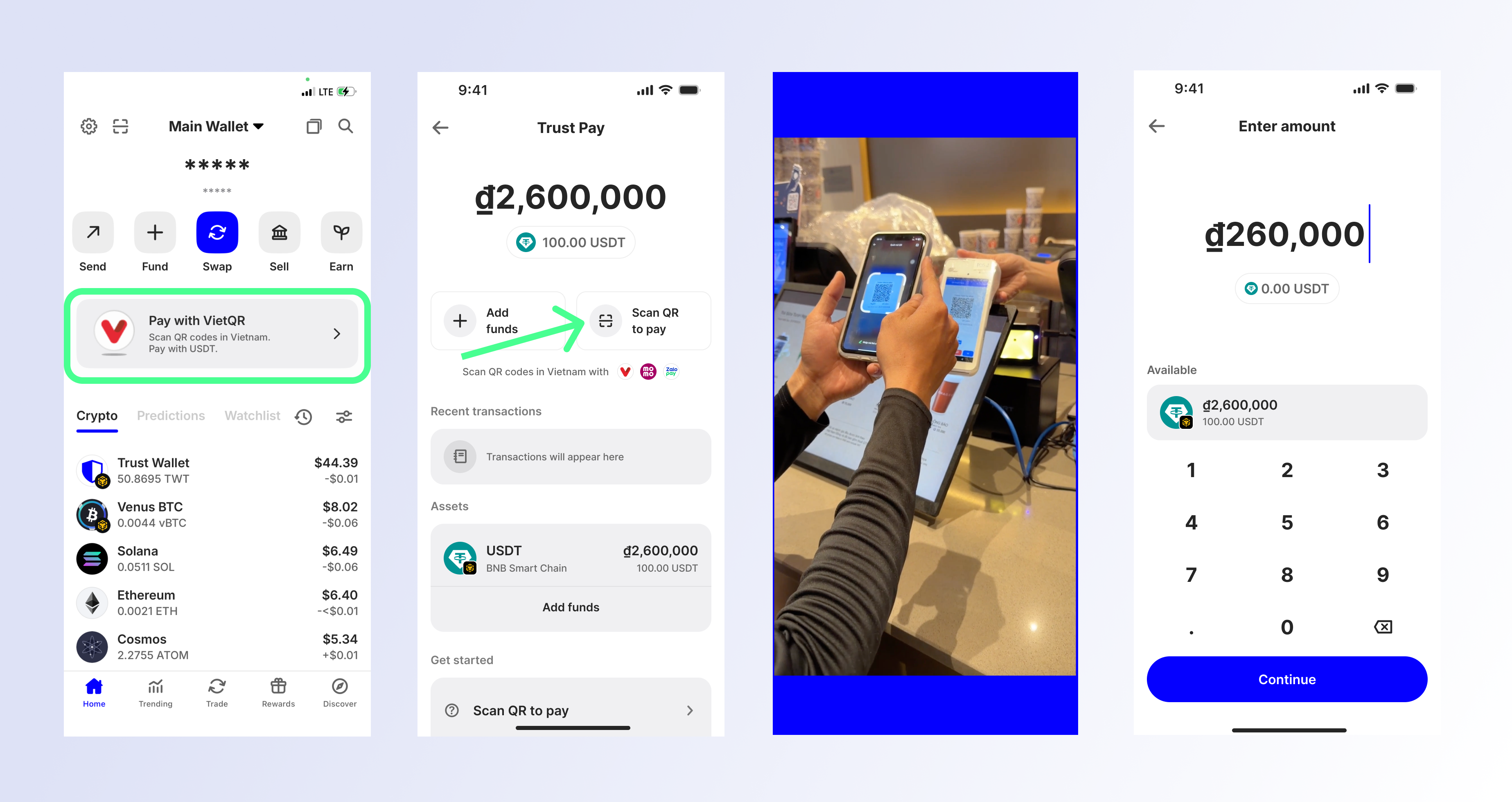

How stablecoin QR settlements work

Stablecoin QR settlements replace the traditional clearinghouse model with a direct on-chain exchange. When a customer scans a merchant’s QR code, the transaction initiates a smart contract execution rather than a bank-to-bank query. This structural shift eliminates the multi-day settlement lag inherent in ACH transfers and the complex fee structures of card networks.

The process relies on the stability of the underlying asset. Unlike volatile cryptocurrencies, stablecoins like USDT are pegged to fiat currencies, ensuring the value received by the merchant matches the value paid by the customer at the moment of scan. This peg stability is critical for small businesses that cannot absorb currency fluctuation risk during the payment window.

The technical flow follows a strict sequence, reducing friction by removing intermediary validation steps. Below is the operational sequence for a standard stablecoin QR transaction.

The merchant displays a dynamic QR code containing the wallet address, currency pair (e.g., USDT/USD), and exact settlement amount. The customer’s wallet app decodes this data, ensuring the payment destination and value are pre-verified before any funds are committed. This encoding step replaces the manual entry required in many legacy systems, reducing input errors.

The customer’s device signs the transaction locally using their private key. This digital signature is broadcast to the blockchain network. Unlike card networks that query bank balances through a centralized switch, the blockchain verifies the sender’s balance and signature validity across distributed nodes. This verification is near-instant, typically completing within seconds rather than the minutes or hours required for traditional authorization.

Once verified, the smart contract executes the transfer. The stablecoin is moved from the customer’s wallet to the merchant’s designated address. Because this occurs on-chain, there is no need for a third-party processor to hold or route the funds. The settlement is final and irreversible at this stage, providing the merchant with immediate proof of payment without the risk of chargebacks common in card-based systems.

The merchant’s backend system receives a notification of the confirmed transaction. The stablecoin is now in the merchant’s possession, fully settled. If the merchant requires fiat currency, they can immediately swap the stablecoin for USD via a regulated exchange or payment processor, locking in the value at the current market rate. This final step closes the loop, allowing the merchant to reconcile the transaction in their accounting software instantly.

This workflow significantly reduces the cost per transaction. Traditional card payments often deduct 2-3% in interchange and processing fees. Stablecoin QR settlements primarily incur network gas fees, which are typically fractions of a cent, regardless of the transaction size. For low-margin retail, this cost structure provides a tangible competitive advantage.

Cost advantages over card networks

Traditional payment processors rely on a layered fee structure that significantly erodes merchant margins. A standard card transaction typically incurs a swipe fee ranging from 1.5% to 3.5%, plus a fixed per-transaction assessment fee and additional cross-border charges. In contrast, stablecoin settlements via QR Pay operate on blockchain networks with minimal gas fees, often totaling less than 1% of the transaction value. This structural difference creates a substantial margin advantage for small businesses, particularly those with low average order values where fixed processing fees disproportionately impact profitability.

The following comparison illustrates the operational cost differences between traditional card networks and stablecoin QR settlements. While card networks charge multiple hidden fees, stablecoin transactions consolidate costs into a single, transparent network fee.

| Metric | Traditional Card Network | Stable QR Pay 2026 |

|---|---|---|

| Processing Fee | 1.5%–3.5% + fixed fee | <0.5% flat fee |

| Settlement Time | 2–3 business days | Seconds to minutes |

| Chargeback Risk | High (dispute-heavy) | Low (irreversible) |

| Cross-Border Cost | 3%–5% + FX spread | Standard network fee |

Beyond direct processing fees, the speed of settlement offers a hidden financial benefit. Traditional card networks hold funds in escrow for days, creating cash flow friction for small merchants who rely on immediate liquidity. Stablecoin settlements provide near-instant finality, allowing businesses to access capital immediately. This reduction in working capital requirements can lower the need for short-term financing or credit lines, further improving the net cost position for small enterprises.

While the initial adoption curve for stablecoin payments requires technical integration, the long-term cost structure is inherently more scalable than legacy card networks. As transaction volumes grow, the fixed costs of card processing remain constant while the relative burden of blockchain fees diminishes. This dynamic makes stable QR Pay particularly attractive for high-volume, low-margin retail environments where every basis point of savings contributes to overall viability.

Adoption hurdles and regulatory risks

While stablecoin QR payments promise lower fees and instant settlement, significant barriers remain for widespread merchant adoption. The primary challenge is regulatory uncertainty. Unlike traditional fiat transactions, which are protected by established banking frameworks, stablecoin settlements operate in an evolving legal landscape. Merchants must navigate varying compliance requirements across jurisdictions, where the classification of digital assets can shift rapidly. Deloitte notes that while digital wallets and QR systems are becoming embedded in daily life, the financial services sector remains cautious about integrating crypto-native rails without clear regulatory guardrails (Deloitte).

Technical friction also poses a substantial hurdle for non-crypto-native businesses. Scanning a QR code involves more steps than a simple NFC tap, creating potential friction at the point of sale. For high-volume environments like grocery stores, this added latency can slow checkout lines and frustrate customers. Additionally, while the QR code itself is a static image, the security of the transaction depends entirely on the underlying wallet infrastructure and the merchant’s ability to verify incoming transactions on the blockchain, a skill set most small business owners do not possess.

Price volatility, though mitigated by stablecoins, is not entirely eliminated. Peg deviations can occur during periods of extreme market stress, exposing merchants to minor but real financial risk if they do not immediately convert holdings to fiat. To monitor these fluctuations, merchants should track the stability of the underlying asset.

The cost-benefit analysis for small businesses must account for these hidden risks. While transaction fees may be lower, the potential costs of regulatory non-compliance, technical integration errors, and customer education can outweigh the savings. Merchants should proceed with caution, prioritizing platforms that offer fiat off-ramps and robust customer support to mitigate these operational risks.

Key questions on QR payment adoption

Stablecoin settlement via QR codes is moving from experimental pilots to established rails, but the transition requires careful evaluation of infrastructure costs and operational friction. The following analysis addresses common inquiries regarding the viability, geographic availability, and limitations of this payment method.

The shift toward stablecoin settlements introduces a layer of complexity. While QR codes provide the user interface, the underlying blockchain settlement must be auditable and compliant. Businesses must weigh the lower transaction fees of crypto rails against the operational overhead of managing digital wallet integrations and ensuring regulatory adherence.

No comments yet. Be the first to share your thoughts!