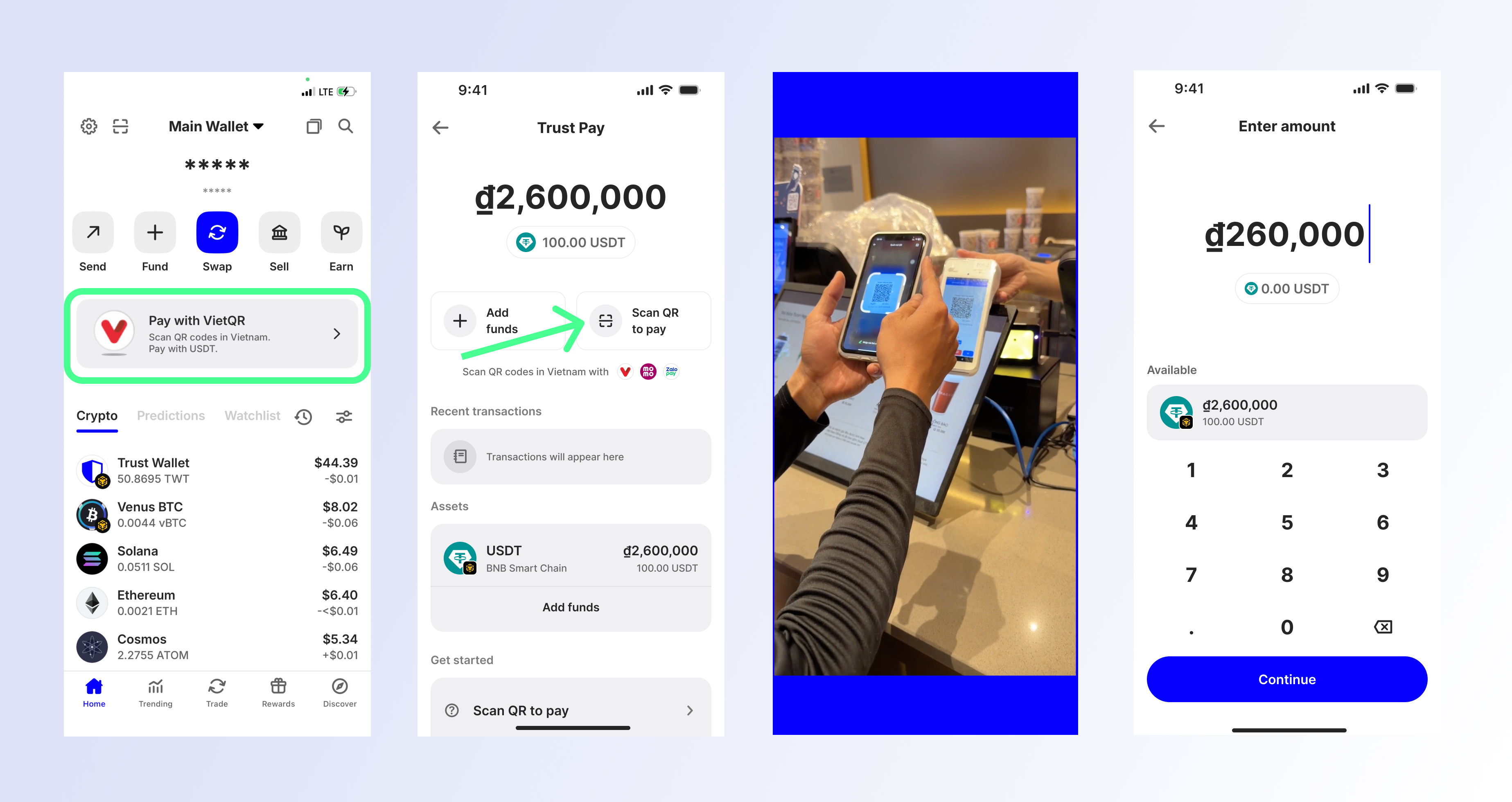

Market shift to stablecoin qr pay

The interface for digital payments has standardized on QR codes, but the settlement layers beneath them are undergoing a quiet consolidation. By 2026, the friction that once defined crypto payments has largely been abstracted away, replaced by infrastructure that mirrors the speed and ubiquity of traditional card networks. This shift is not merely technological; it represents a structural change in how value moves across borders and between merchants and consumers.

The scale of this transition is measurable. Global QR code-based payment markets, valued at $16.7 billion in 2025, are projected to reach $19.8 billion in 2026, with retail QR transactions expected to constitute half of all wallet payments within five years. This growth is driven by the convergence of mobile penetration and the need for low-cost, instant settlement rails. For merchants, the appeal lies in the elimination of chargeback risk and the reduction of intermediary fees, while consumers benefit from the speed of on-chain finality.

However, the dominance of the QR interface masks a complex backend. Providers like Coinbase Payments, built on Ethereum Layer-2 networks such as Base, are centralizing the complexity of stablecoin transactions. These platforms abstract the blockchain mechanics, allowing businesses to accept USDT or USDC without managing private keys or navigating gas fees directly. This consolidation creates a more uniform user experience but introduces a new dependency on a smaller set of infrastructure providers who control the settlement logic.

The stability of these assets during market volatility is critical to their adoption as a payment medium. Unlike volatile cryptocurrencies, stablecoins pegged to fiat currencies offer the predictability required for daily commerce. The following chart illustrates the tight peg of USDT to USD, demonstrating the reliability of these assets even during periods of broader market stress.

Top stablecoin payment providers

The infrastructure for stablecoin QR settlement is consolidating around a handful of providers that can handle the dual demands of blockchain finality and fiat reconciliation. For merchants, the choice is no longer about which chain to use, but which settlement layer offers the necessary liquidity and compliance guardrails. The current market is dominated by four distinct players: Cobo, Circle, Stripe, and Coinbase, each approaching the problem from a different architectural angle.

Cobo operates as a multi-chain liquidity aggregator, positioning itself as the connective tissue between disparate networks. Its value proposition lies in its ability to abstract the underlying blockchain complexity, allowing merchants to accept payments on multiple chains while settling in a single preferred asset. This is particularly relevant for merchants in emerging markets where USDT dominance on Tron or BSC is higher than Ethereum-based stablecoins. Cobo’s infrastructure is built to handle high-volume, low-margin transactions by optimizing gas costs and providing real-time liquidity routing.

Circle, the issuer of USDC, offers a more integrated approach by leveraging its native position in the stablecoin ecosystem. Circle’s payment solutions are designed to minimize settlement risk by utilizing its own issuance and redemption rails. For merchants concerned with regulatory clarity and asset backing, Circle provides a direct line to the issuer. This vertical integration reduces counterparty risk but can limit flexibility if a merchant wishes to diversify across other stablecoins like USDT or DAI. The trade-off is a streamlined, compliant experience that may lack the multi-chain flexibility of aggregators.

Stripe and Coinbase represent the legacy fintech and crypto-native approaches, respectively. Stripe’s entry into stablecoin payments is characterized by its deep integration with existing merchant acquirers and its focus on seamless fiat off-ramps. It appeals to merchants who want to maintain their current operational workflows while adding crypto as a payment option without managing private keys or exchange relationships. Coinbase, through its Coinbase Payments platform, leverages its Ethereum Layer-2 network, Base, to offer low-cost, fast settlements. This is ideal for merchants already embedded in the Coinbase ecosystem or those targeting crypto-native customers who prefer using Base for its speed and cost efficiency.

The following comparison highlights the core operational differences between these providers.

Settlement speed and cost analysis

The technical infrastructure underlying a QR transaction determines the merchant’s actual exposure to risk and the efficiency of their capital. When a customer scans a code, the transaction must propagate through a blockchain network, achieve finality, and settle into the merchant’s wallet. The choice of network—whether Solana, Base, or Polygon—creates distinct tradeoffs between speed, cost, and security guarantees that directly impact cash flow.

Base, Coinbase’s Ethereum Layer-2 network, offers a balanced approach for merchants seeking Ethereum-level security with significantly lower costs. Transactions on Base typically settle within seconds and cost fractions of a cent, making it suitable for high-volume, low-margin QR payments. However, merchants must understand that finality on Layer-2 solutions is not instantaneous; it relies on sequencers and periodic settlement on the Ethereum mainnet. This introduces a slight delay compared to native Layer-1 chains, though for most retail transactions, this delay is imperceptible to the end user.

Solana provides the fastest finality among major stablecoin networks, often processing transactions in sub-second intervals. Its low fees make it attractive for micro-transactions, but the network has historically experienced outages. For high-stakes merchant settlement, this reliability variance requires careful risk assessment. Polygon, another Ethereum-compatible Layer-2, offers similar cost structures to Base but with a different validator set and finality model. Merchants should compare the specific finality guarantees of each provider’s implementation, as "instant" often means "pending Layer-2 finality" rather than absolute on-chain confirmation.

| Network | Approx. Finality | Avg. Fee |

|---|---|---|

| Base | 1-3 seconds | <$0.01 |

| Solana | <1 second | <$0.01 |

| Polygon | 2-5 seconds | <$0.01 |

The choice is not merely technical but strategic. Merchants processing high volumes of small payments benefit most from networks with the lowest per-transaction fees, even if finality is marginally slower. Conversely, merchants handling large, infrequent transactions may prioritize networks with the strongest security guarantees, even at a slightly higher cost. Understanding these nuances allows businesses to select a settlement rail that aligns with their operational needs and risk tolerance.

Regional adoption and compliance risks

The rollout of stablecoin QR payments is proceeding at uneven speeds across different geographies, creating a fragmented landscape for merchants. While some regions are integrating these systems into existing mobile money infrastructures, others are grappling with regulatory uncertainty or provider instability. For cross-border operators, this variance introduces significant compliance overhead and operational risk that cannot be ignored.

In Southeast Asia, adoption is driven by high mobile penetration and a desire for faster settlement. Vietnam has emerged as a testing ground for QR-based stablecoin transactions, leveraging its existing infrastructure for rapid domestic payments. Similarly, the Philippines is seeing increased integration of crypto-adjacent payment rails, though regulatory clarity remains a moving target. Merchants in these markets must navigate local central bank guidelines that often lag behind technological innovation.

Africa presents a different use case, focusing on cross-border trade and financial inclusion. SQRIL recently expanded its API to support stablecoin-to-fiat QR transactions in Tanzania, Kenya, and South Africa. This integration allows merchants to accept digital assets and settle in local fiat currency, reducing the friction of currency conversion. However, the reliance on third-party payment providers in these emerging markets requires rigorous due diligence regarding their longevity and regulatory standing.

The fragility of the provider ecosystem is a critical risk factor. In March 2026, Trust Wallet announced the temporary discontinuation of its QR Payments feature due to changes in its underlying payment provider. This move underscores the volatility inherent in relying on non-bank financial intermediaries for core settlement infrastructure. Merchants integrating these solutions must verify the longevity and regulatory compliance of their payment processors to avoid sudden service interruptions.

Compliance across borders requires a multi-layered approach. Merchants operating in multiple regions must adhere to the strictest anti-money laundering (AML) and know-your-customer (KYC) standards applicable to their jurisdiction. This often means implementing different verification protocols for domestic versus international QR transactions. Failure to align with local regulatory frameworks can result in frozen assets or legal penalties, making compliance a non-negotiable cost of doing business in the stablecoin payment space.

Choosing the right QR pay provider

Selecting a stablecoin settlement rail requires aligning technical infrastructure with volume thresholds and regulatory exposure. The decision framework rests on three variables: transaction velocity, geographic jurisdiction, and internal engineering capacity. Providers that abstract blockchain complexity, such as Coinbase Payments on Base, suit merchants lacking dedicated crypto engineering teams, while high-volume enterprises often require direct custody solutions like Fireblocks or Cobo to manage multi-chain liquidity and audit trails.

Volume dictates the cost structure. Low-volume merchants benefit from hosted payment gateways that handle compliance and settlement automatically, absorbing the technical overhead for a higher per-transaction fee. High-volume operators, however, must evaluate the marginal cost of on-chain settlement versus centralized processing. For these merchants, the reliability of the underlying settlement rail becomes the primary metric, outweighing convenience features.

Geographic location determines which stablecoins are legally permissible and which fiat off-ramps are accessible. A provider’s ability to offer localized settlement in USD, EUR, or local currencies directly impacts merchant adoption and liquidity risk. Merchants in jurisdictions with strict stablecoin regulations must prioritize providers with explicit licensing and transparent reserve auditing.

Technical capacity is the final filter. If your team cannot maintain private key management or monitor gas fees across multiple chains, you must choose a provider that offers institutional-grade custody and automated reconciliation. The right provider reduces settlement friction to a background process, allowing your business to focus on revenue rather than blockchain mechanics.

Common questions about stablecoin QR pay

Digital payment methods have rapidly gained popularity since 2020, a trend that is likely to continue as more merchants choose QR code options to make payments faster and safer. However, the infrastructure supporting these transactions is not static. Notice that QR Payments will be temporarily discontinued on March 31, 6AM UTC, 2026, due to changes in the payment provider, highlighting the fragility of relying on single-point integrations.

The role of the payment service provider is central to this ecosystem. Coinbase operates Coinbase Payments, a full-stack stablecoin payment solution built on its Ethereum Layer-2 network, Base. This platform abstracts blockchain complexity so businesses can offer crypto-native payments without specialized teams, though merchants must weigh this convenience against the risk of provider dependency.

No comments yet. Be the first to share your thoughts!