5 Reasons Stable QR Pay Is the 2026 Shift for Small Business

Stable QR payments eliminate the 2.9% + $0.30 friction of traditional card processing, turning a $50 transaction into a net $1.50 savings. By leveraging official protocols from providers like Trust Wallet and RedotPay, small businesses can reduce operational risk while capturing the efficiency gains defining the 2026 financial landscape.

-

Eliminating chargeback fraud risks

Stable QR payments remove the card network’s dispute layer, shifting liability away from merchants. When a customer scans a wallet address, the transaction is immutable, preventing fraudulent "friendly fraud" claims that typically cost small businesses hundreds in chargeback fees. This structural change protects revenue integrity without requiring expensive third-party fraud detection tools or manual review processes for every single transaction. -

Reducing merchant processing fees

Traditional card processors charge 2.9% plus $0.30 per transaction, eating into thin margins. Stable QR systems often cap fees near 1% or offer flat-rate micro-transfers, saving approximately $1.50 on a $50 sale. By bypassing Visa and Mastercard interchange networks, merchants retain more capital for inventory and growth, transforming payment costs from a variable expense into a predictable, minimal overhead line item. -

Instant settlement for cash flow

Unlike card networks that hold funds for two to three business days, stablecoin settlements occur on-chain within seconds. This immediacy provides real-time liquidity, allowing businesses to pay suppliers or restock inventory immediately after a sale. The reduction in cash flow lag eliminates the need for short-term bridging loans, significantly improving working capital efficiency and reducing interest expenses associated with delayed revenue recognition. -

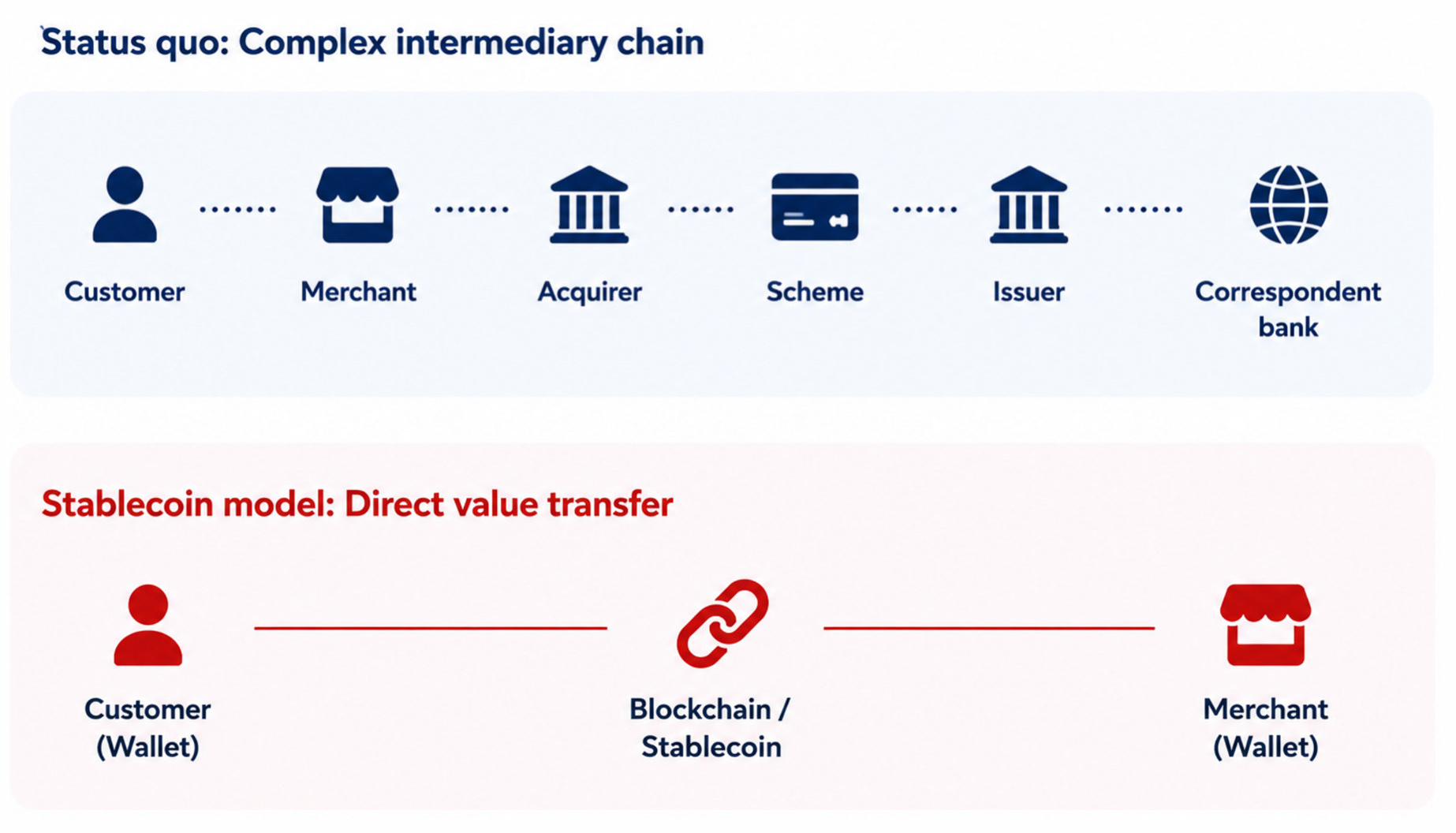

Bypassing traditional banking delays

Cross-border bank transfers often involve correspondent banks and SWIFT networks, introducing multi-day delays and hidden intermediary fees. Stable QR payments settle directly on the blockchain, bypassing these legacy financial intermediaries entirely. This direct peer-to-peer settlement ensures that international vendors receive funds instantly, regardless of time zones or national banking holidays, streamlining global supply chain operations and reducing administrative friction. -

Simplifying cross-border payment compliance

Managing multi-currency accounts requires significant administrative overhead and regulatory scrutiny under traditional banking frameworks. Stable QR payments utilize pegged assets like USDC, maintaining a consistent value reference that simplifies accounting and tax reporting. By standardizing the settlement currency, businesses reduce the complexity of foreign exchange hedging and comply with anti-money laundering protocols through transparent, auditable on-chain transaction records provided by compliant gateways.

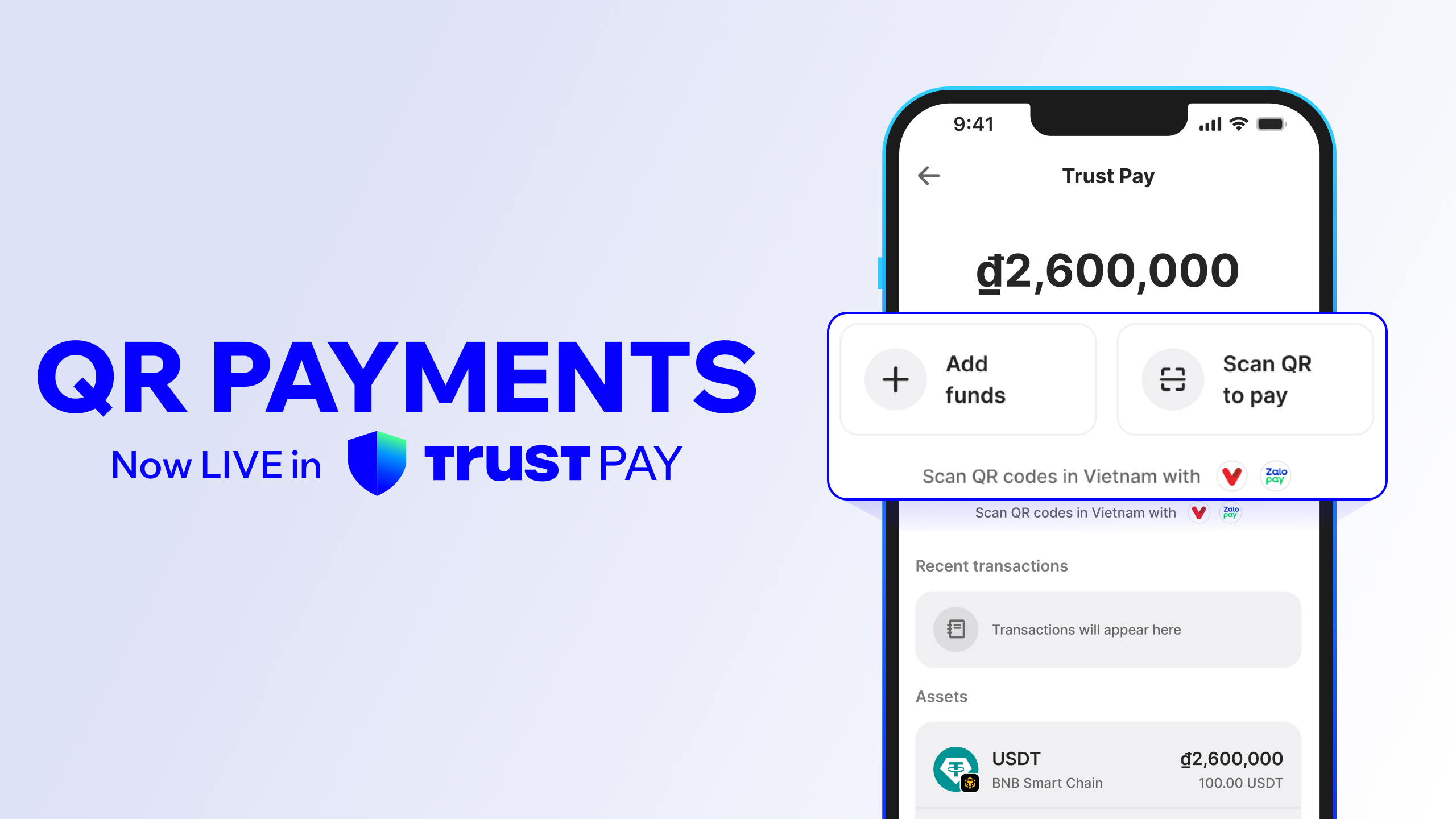

Instant fiat settlement removes volatility risk

The primary barrier for small merchants adopting digital assets has always been price volatility. Stable QR Pay solves this by handling the conversion backend, ensuring the business receives predictable local currency rather than fluctuating crypto tokens. When a customer scans a QR code, the system automatically converts the stablecoin to fiat in the background before the funds hit the merchant's account.

This mechanism effectively isolates the merchant from the crypto market's turbulence. According to Trust Wallet, merchants receive local currency instantly while the customer remains self-custodial, eliminating the need for the business to manage crypto wallets or hedge against price drops. Similarly, Bitget notes that this "last mile" conversion happens seamlessly during the scan, meaning the merchant never actually holds the volatile asset.

For operational efficiency, this translates to predictable cash flow. A $50 sale yields exactly $50 in the bank, regardless of whether the underlying stablecoin dips or spikes by 1% in the seconds it takes to settle. This stability allows small businesses to price goods and manage inventory without the anxiety of overnight crypto market swings.

The technical reliability of this rail is best observed in the stability of the assets themselves. Unlike volatile cryptocurrencies, stablecoins like USDT or USDC maintain a peg to the dollar, providing the consistent settlement layer that traditional card networks have long offered.

Lower fees replace traditional merchant discount rates

Small businesses operate on thin margins, where every percentage point of processing cost eats directly into profit. Traditional credit card networks typically charge a merchant discount rate (MDR) of 1.5% to 3.5%, plus a fixed per-transaction fee. For a $50 sale, this standard model deducts approximately $1.50 to $2.00 in fees. Over hundreds of low-ticket transactions, these costs accumulate, eroding the viability of small-scale retail and service operations.

Stable QR payments disrupt this cost structure by leveraging blockchain settlement layers that bypass traditional interchange networks. Providers like Ripe facilitate direct peer-to-peer transactions, reducing the fee layer to a flat rate or a percentage often below 1%. On the same $50 transaction, a 0.5% fee results in a cost of just $0.25. This represents a savings of $1.25 to $1.75 per sale, preserving margin that would otherwise be lost to financial intermediaries.

The difference becomes critical when analyzing volume. A coffee shop processing 200 transactions daily at an average ticket of $5 faces significant annual fee burdens under traditional models. Switching to stable QR payments shifts these costs from a variable percentage to a predictable, minimal flat fee or negligible percentage. This operational efficiency allows businesses to reinvest savings into inventory, labor, or customer experience rather than paying rent to payment processors.

| Fee Structure | Traditional Credit Card | Stable QR Pay |

|---|---|---|

| Typical Rate | 2.9% + $0.30 per transaction | 0.1% - 1% (or flat fee) |

| $50 Sale Cost | ~$1.75 | ~$0.05 - $0.50 |

| $5 Sale Cost | ~$0.45 | ~$0.005 - $0.05 |

Source: Comparative analysis of standard merchant processing rates vs. stablecoin settlement models (e.g., Ripe).

Beyond immediate cost savings, the predictability of stable QR fees aids in financial planning. Merchants can forecast net revenue with greater accuracy, as fees no longer fluctuate with card network interchange adjustments. This transparency supports better cash flow management, a critical factor for small businesses navigating economic volatility.

Frictionless checkout speeds up customer flow

Scanning a QR code removes the mechanical delays inherent in traditional card terminals. A customer no longer needs to wait for a card reader to boot, insert a chip, or wait for a signature. Instead, they simply open their wallet app and scan. This reduces the average transaction time to a few seconds, keeping lines moving during peak hours.

The operational impact is measurable. During busy periods, reduced queue times mean higher table turnover for restaurants or more customers served at retail counters. This efficiency directly supports revenue without requiring additional staff. The speed advantage is particularly pronounced for small-ticket items, where the overhead of card processing often outweighs the benefit of the sale itself.

Stablecoin payments also eliminate the risk of card fraud and chargebacks associated with magnetic stripe transactions. By bypassing the card networks entirely, merchants avoid the associated chargeback disputes and the time spent managing them. The transaction is final upon confirmation, providing immediate certainty.

For a $50 sale, the fee savings from avoiding card processing can amount to $1.50 or more per transaction. When multiplied across hundreds of daily sales, these savings accumulate significantly. RedotPay’s scan-to-pay feature demonstrates this efficiency by enabling instant stablecoin transfers that settle quickly, mirroring the speed of cash without the physical handling risks.

Global acceptance expands the customer base

Stable QR payments remove the friction of international transactions, allowing small businesses to accept funds from tourists and cross-border customers without the overhead of currency exchange. Unlike traditional card networks that levy foreign transaction fees, stablecoin QR systems settle directly in digital dollars, effectively eliminating the 1-3% surcharge typically applied to international purchases.

The operational efficiency is measurable. On a $50 sale, a merchant using a traditional processor might lose $1.50 to foreign exchange spreads and processing fees. With stable QR, that margin is preserved. The customer pays from their existing wallet, and the system handles the backend conversion to local fiat if needed, ensuring the merchant receives the full agreed-upon amount.

This approach is particularly effective in high-tourism regions. Services like Stables provide compliant APIs that enable merchants to accept USDT instantly across borders. For technical implementation, providers such as Trust Wallet and RedotPay offer documentation on integrating these payment rails, ensuring that the transaction remains transparent and auditable. By adopting this method, businesses reduce the risk of chargebacks associated with cross-border disputes while expanding their addressable market.

Self-custody reduces chargeback fraud exposure

Card networks operate on a reversible ledger, meaning a merchant can be forced to return funds long after a sale is complete. This mechanism enables "friendly fraud," where customers dispute legitimate transactions to retain both goods and money. For small businesses, these chargebacks are not just lost revenue; they trigger additional penalty fees and can jeopardize merchant account standing.

Stablecoin QR payments shift this risk profile. Because blockchain transactions are irreversible, the merchant retains the funds once the block is confirmed. There is no central authority to reverse the transfer based on a customer's claim. This irreversibility acts as a final settlement layer, eliminating the administrative burden and financial loss associated with disputed card transactions.

Consider a standard $50 retail sale. In a card-based system, the merchant pays interchange fees and faces the risk of a chargeback that could cost the full $50 plus a $25 dispute fee. With stablecoin QR payments, the $50 is received instantly and cannot be clawed back. The merchant saves the interchange fee (often 1.5% to 3.5%) and eliminates the fraud exposure entirely.

This operational efficiency is central to the value proposition of self-custodial wallets. As noted in Trust Wallet's official documentation on QR payments, merchants receive local currency instantly while maintaining full control over their assets [src-serp-1]. The technology removes the intermediary that typically facilitates fraud disputes, streamlining the flow of capital.

By adopting stablecoin QR infrastructure, businesses convert a variable risk (chargebacks) into a fixed, known cost (network fees). This predictability allows for tighter margin management and reduces the need for costly fraud detection software commonly required by traditional payment processors.

No comments yet. Be the first to share your thoughts!