What stable QR pay actually does

Stable QR pay sits at the intersection of two distinct technologies: the QR code scanning infrastructure already present in most point-of-sale systems, and the blockchain rails that settle the transaction. The innovation isn't the barcode itself—it's the asset moving through it. By using a stablecoin as the settlement layer, merchants bypass the traditional card network entirely, receiving funds directly into a digital wallet rather than waiting for bank transfers.

This model shifts the value proposition from convenience to economics. While traditional QR payments often rely on local payment switches or bank APIs that still incur interchange fees, stablecoin QR payments settle on-chain. For the merchant, this means the cost of accepting a payment drops significantly, often to a fraction of a cent, regardless of the transaction size. The QR code is simply the trigger; the stablecoin is the engine.

Trust in this system rests on the stability of the settlement asset. Merchants need to know that the value they receive today is the value they get tomorrow, without exposure to the volatility of assets like Bitcoin or Ethereum. This is why USDC and similar regulated stablecoins are the standard for this infrastructure. They provide the speed of crypto with the predictability of fiat.

The image below illustrates how this infrastructure appears in the real world. A simple QR sign on a storefront window acts as the gateway, replacing the physical card terminal. The customer scans, approves the transaction in their wallet, and the merchant receives the stablecoin instantly. It is a seamless handoff between the physical and digital economies.

Why instant settlement changes merchant math

Traditional card payments operate on a T+2 settlement cycle. This means the money a customer spends does not hit the merchant’s bank account for two to three business days. That delay creates a working capital drag. For small businesses with tight cash flow, waiting days to access revenue from yesterday’s sales can limit the ability to restock inventory or cover immediate operational costs.

Instant settlement via stable QR payments removes this lag. Funds are available immediately, allowing merchants to reinvest capital without relying on credit lines or savings buffers. This liquidity shift directly improves operational flexibility and reduces the friction of daily financial management.

Beyond timing, the settlement speed alters the risk profile of each transaction. In the traditional card ecosystem, the window for chargebacks remains open for weeks or even months after a purchase. This uncertainty forces merchants to hold reserves or absorb losses from fraudulent disputes. Stable QR payments, by contrast, offer near-instant finality. While fraud prevention remains essential, the extended chargeback window characteristic of card networks is significantly reduced or eliminated, protecting net revenue from post-transaction reversals.

To understand the broader financial context, consider how traditional payment rails compare to instant alternatives in terms of cost and speed.

| Feature | Traditional Card | Stable QR Pay |

|---|---|---|

| Settlement Time | T+2 to T+3 days | Instant |

| Chargeback Window | Up to 120 days | Minimal/None |

| Working Capital | Delayed access | Immediate access |

This structural difference means that for every dollar earned, the merchant retains control and liquidity faster. The combination of reduced fees and immediate access to funds creates a compounding effect on profitability that static pricing models often fail to capture.

How merchants accept stablecoin payments

The operational workflow for stablecoin transactions mirrors the familiar experience of scanning a QR code at a coffee shop or retail counter. For the customer, the process begins by opening a compatible digital wallet and scanning the merchant’s dynamic QR code. This code contains the payment address and the exact amount owed, ensuring precision and reducing manual entry errors. The transaction is then broadcast to the blockchain network, where it is confirmed within seconds. This speed allows merchants to verify payments almost instantly, eliminating the multi-day settlement periods typical of traditional card networks.

Behind the scenes, the complexity lies in how the merchant handles the incoming asset. There are two primary approaches: holding the stablecoin or converting it immediately. Merchants who choose to hold stablecoins can retain exposure to the digital asset, potentially benefiting from cross-border efficiency or future yield opportunities. However, many businesses prefer to mitigate volatility risk by using payment processors that automatically convert the received stablecoin into local fiat currency. This backend conversion ensures that the merchant receives the exact value owed in their preferred currency, effectively neutralizing market fluctuations while still enjoying the lower transaction fees of blockchain settlements.

Integration with existing point-of-sale (POS) systems is designed to be seamless. Most modern payment gateways offer plugins or APIs that allow merchants to display a QR code directly on their current checkout interface. This means there is no need to replace hardware or retrain staff extensively. The customer simply scans the screen, confirms the payment in their wallet, and the POS system registers the success. This low-friction adoption model lowers the barrier to entry, allowing small and medium-sized businesses to offer instant settlement options without significant technical overhead.

Real-world adoption in emerging markets

Stable QR pay has moved beyond pilot programs into daily commerce across Southeast Asia, where established national QR standards are being adapted for stablecoin settlements. In these markets, the technology solves a specific friction point: merchants receive local fiat currency instantly, while consumers pay with self-custodied stablecoins. This hybrid model allows users to bypass traditional card networks and their associated interchange fees without requiring merchants to hold volatile crypto assets.

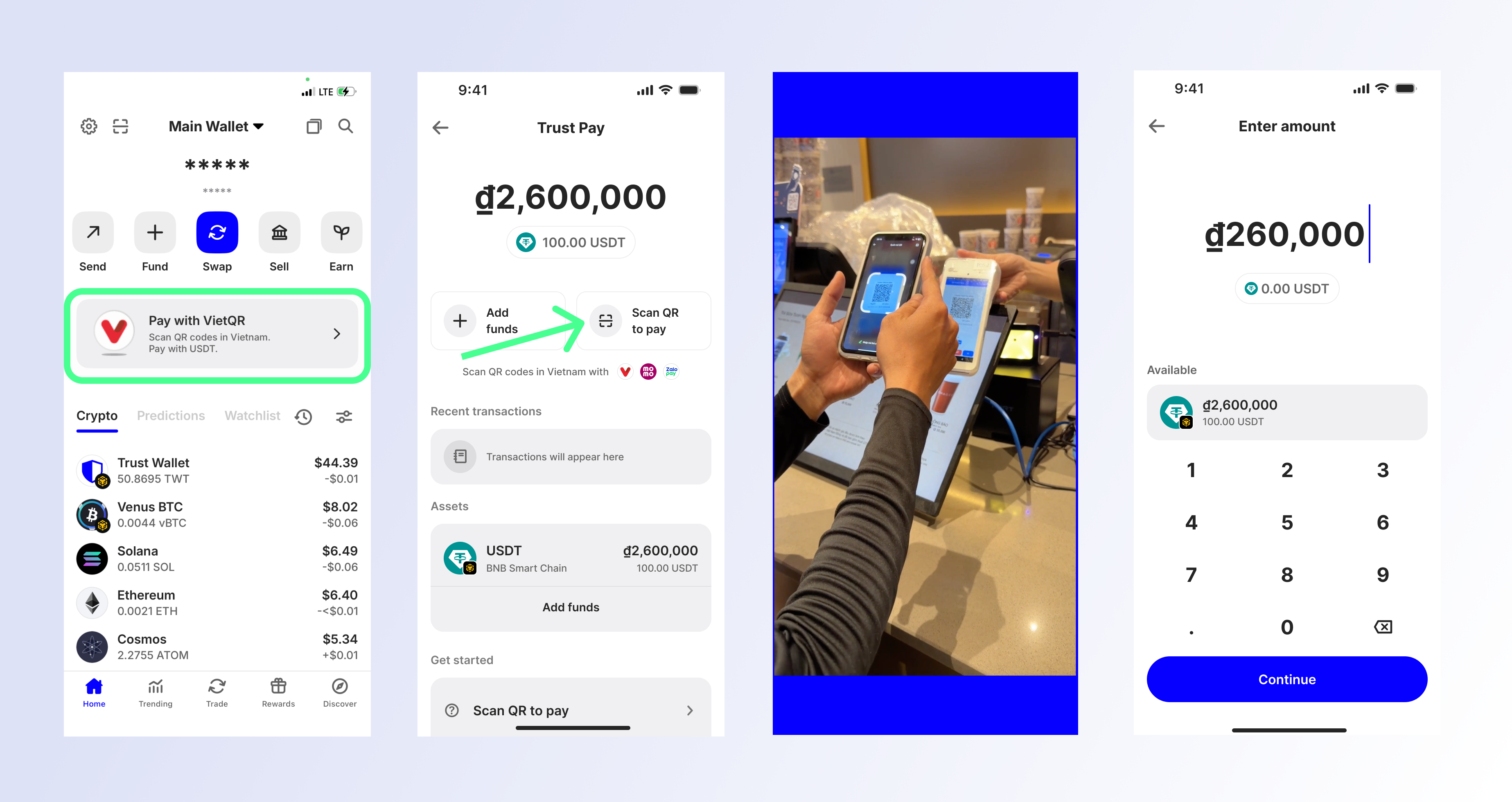

In Vietnam, the VietQR standard has become the backbone of digital payments. Providers like RedotPay have integrated stablecoin payments directly into this existing infrastructure. Users can scan a merchant’s VietQR code using a compatible wallet, and the system automatically converts the stablecoin payment into Vietnamese dong for the merchant. This seamless conversion happens in real-time, ensuring the merchant is insulated from cryptocurrency price fluctuations while the payer benefits from lower transaction costs and faster settlement times.

The Philippines offers a similar landscape with PromptPay and EMV QR standards. Here, stable QR pay allows consumers to spend USDT or USDC at any merchant accepting the national QR code. The underlying technology links the stablecoin transaction to the merchant’s bank account or e-wallet, effectively bridging the gap between decentralized finance and the traditional banking system. This adoption is critical for the unbanked and underbanked populations who rely on mobile money for their daily transactions.

The value of these transactions is anchored by the stability of the underlying assets. As stablecoins like USDT and USDC maintain their peg, they provide a reliable medium of exchange in economies where local currency volatility can erode purchasing power. The following widget shows the current market price of USDT, reflecting the stability that makes these instant settlements viable for everyday commerce.

Key risks and compliance considerations

Instant settlement is powerful, but it doesn't exempt merchants from the heavy lifting of financial regulation. Unlike traditional credit card networks that absorb chargeback risk and handle compliance layers, crypto payments place the burden of verification squarely on the merchant. To accept stablecoin payments safely, you must navigate a complex web of KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements.

The first line of defense is choosing the right infrastructure. Not all stablecoins are created equal. Using regulated stablecoin issuers like USDC or USDT ensures that the asset backing your settlement is transparent and auditable. This reduces the risk of holding depegged or fraudulent tokens. Always verify the issuer's regulatory status in your jurisdiction before integrating their payment rails.

Beyond the token itself, your payment processor must support robust transaction monitoring. QR code payments are fast, but they can also be exploited for illicit activities if not properly screened. Ensure your provider flags suspicious patterns, such as rapid-fire small transactions or connections to darknet markets. This proactive stance protects your merchant account from being frozen by banking partners.

Finally, keep your legal counsel in the loop. Cryptocurrency regulations vary wildly by region. What is compliant in one country may be illegal in another. Regularly audit your compliance procedures to stay ahead of evolving laws. Treating crypto payments as a standard financial service, rather than a tech novelty, is the best way to mitigate risk and ensure long-term stability.

No comments yet. Be the first to share your thoughts!