What stable qr pay 2026 means for merchants

Stable QR pay 2026 refers to the integration of stablecoin payments into point-of-sale QR code systems, enabling immediate transaction finality for merchants. Unlike traditional card networks, which rely on multi-day clearing cycles and complex intermediary routing, this approach uses blockchain infrastructure to settle funds directly into a merchant’s digital wallet. The result is a payment rail that operates 24/7 with near-instant confirmation, removing the temporal friction inherent in legacy banking systems.

The economic advantage lies in the elimination of interchange fees and network assessment charges. Card processors typically deduct 1.5% to 3.5% per transaction, plus fixed per-transaction fees. Stable QR pay 2026 models often charge only the network gas fee or a minimal flat processing rate, significantly reducing the cost of acceptance. This shift transforms payment processing from a revenue stream for card networks into a low-cost utility for merchants, particularly benefiting high-volume or low-margin businesses.

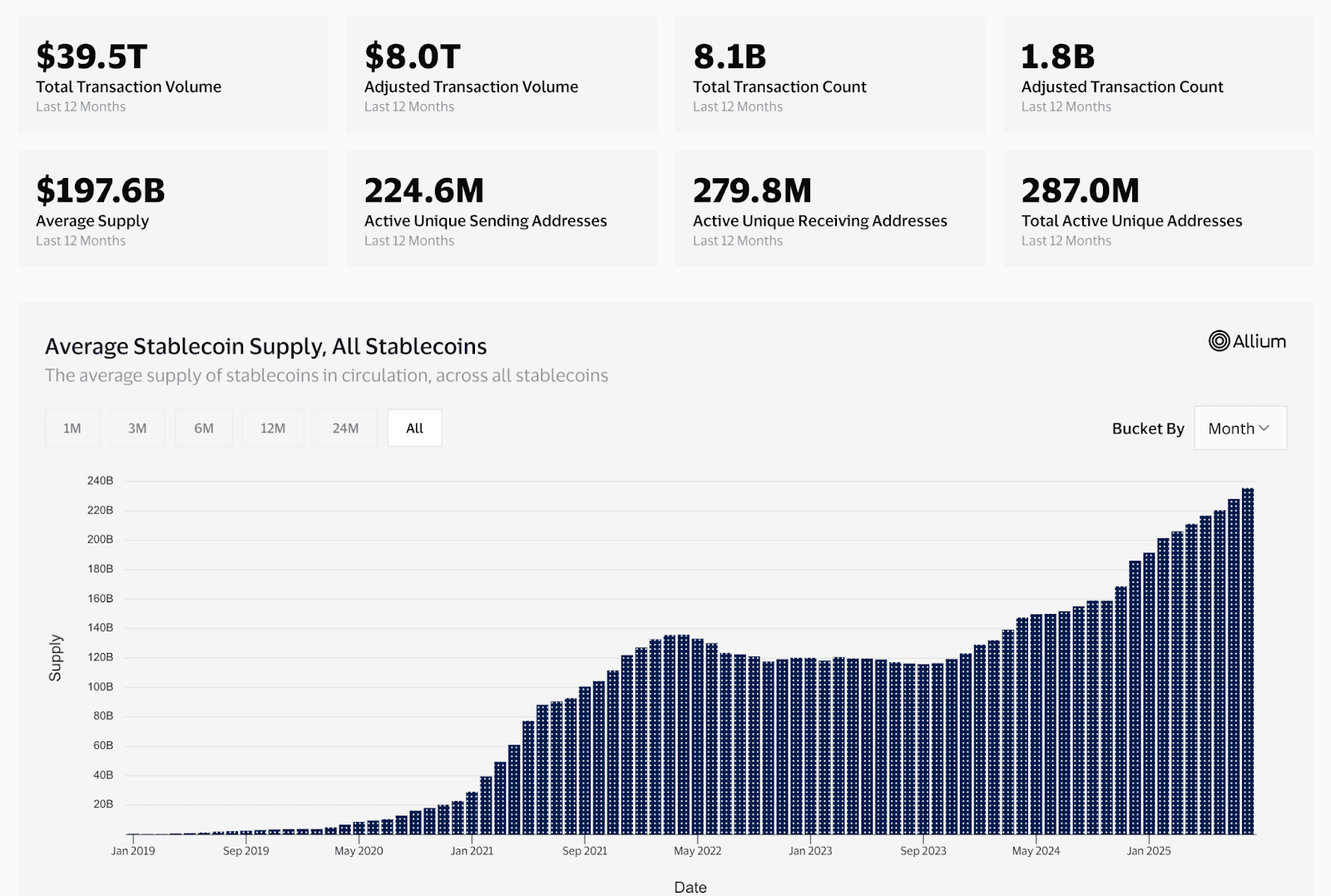

Market data supports the rapid adoption of QR-based payment rails. Juniper Research projects that the value of QR code payments will grow by 50% globally from $5.4 trillion in 2025, exceeding $8 trillion by 2029. This growth is driven by the scalability of QR technology, which requires no specialized hardware beyond a smartphone or basic scanner. As stablecoin infrastructure matures, the convergence of QR scanning and stablecoin settlement offers a unified global standard, bypassing regional card network fragmentation.

KeyTakeaways items=["Stable QR pay 2026 enables instant settlement via blockchain, bypassing card network delays.", "Merchants save on interchange fees, paying only minimal network or processing costs.", "QR code payments are projected to exceed $8 trillion globally by 2029, driven by scalability and low hardware requirements."]

How instant stablecoin settlement works

The technical flow for stable qr pay 2026 replaces the traditional card authorization loop with a direct on-chain transfer. Instead of waiting days for bank clearing, the merchant receives the fiat-equivalent stablecoin immediately upon transaction confirmation. This shift removes the intermediary delays that define legacy payment rails.

The process begins when the customer scans a dynamic QR code at the point of sale. This code contains structured payment data, often adhering to emerging standards like X9.150, which ensures the merchant’s wallet address and the exact stablecoin amount are encoded securely. The customer’s wallet app reads this data and prepares the transaction.

Once the customer confirms the payment, their wallet signs the transaction cryptographically. This signature proves ownership of the funds without revealing sensitive account details. The signed transaction is then broadcast to the underlying blockchain network for validation.

The blockchain network validates the signature and checks for sufficient balance. Once the block is confirmed, the stablecoin is transferred to the merchant’s wallet. The merchant’s payment processor or banking partner then recognizes this on-chain receipt as a completed settlement, effectively converting the digital asset into spendable fiat-equivalent value instantly.

The customer points their wallet at the merchant’s QR code. The code encodes the recipient’s public address and the precise stablecoin amount, ensuring no manual entry errors occur.

The customer’s wallet app prepares the transfer and requests a digital signature. This step verifies the user’s identity and authorizes the specific amount to be moved from their wallet.

The signed transaction is broadcast to the network. Validators confirm the signature and balance, adding the transaction to a new block. This replaces the hours-long authorization hold of card networks.

The stablecoin lands in the merchant’s wallet. The merchant’s backend system recognizes the on-chain event as a settled payment, allowing immediate reconciliation and settlement.

Comparing stable qr pay 2026 options

The stable qr pay 2026 landscape is defined by three distinct approaches: direct wallet integration, bank-led rails, and third-party aggregators. While the underlying technology—converting stablecoin balances into fiat settlements for merchants—remains similar, the user experience and cost structures differ significantly.

Direct wallet solutions, such as those historically offered by Trust Wallet, prioritize self-custody and lower fees by bypassing traditional banking intermediaries. However, this model requires merchants to adopt specific infrastructure. In contrast, bank-led rails like those tested in Vietnam integrate with existing point-of-sale (POS) systems, offering higher merchant adoption but potentially higher settlement fees due to legacy processing layers.

Third-party aggregators sit in the middle, supporting multiple chains and fiat currencies through a single API. This flexibility comes at the cost of transparency; users often cannot see exactly which chain is being used for each transaction or what the exact settlement time is.

The following comparison outlines the primary tradeoffs between these models as they stand in 2026. Focus on fees and supported regions when selecting a provider, as these factors directly impact both merchant profitability and user accessibility.

| Provider Type | Estimated Fees | Supported Chains | Key Regions |

|---|---|---|---|

| Direct Wallet | 0.5-1.0% | USDT, USDC, DAI | Global (Self-Custody) |

| Bank-Led Rail | 1.5-2.5% | N/A (Fiat Only) | Vietnam, Southeast Asia |

| Aggregator | 1.0-2.0% | Multi-chain | Europe, LATAM |

Zero fee qr payments vs traditional rails

The economic advantage of stable qr pay 2026 lies in the fee structure. Traditional card networks charge merchants 2% to 3% per transaction. This includes interchange fees paid to issuing banks and network assessment fees. For small-ticket items, these costs often erase profit margins entirely. Stablecoin QR payments operate on a different model. Transactions settle on-chain or via stablecoin rails with fixed, minimal gas or processing fees. The difference is not marginal; it is structural.

Card fees scale with the transaction amount. A $100 payment loses $2 to $3. A $1 payment loses $0.20 to $0.30. Stablecoin transaction costs remain relatively flat regardless of ticket size. This makes them particularly efficient for microtransactions and high-volume retail. Merchants retain more capital, which can be reinvested or passed to consumers as lower prices. The savings are immediate and visible on every invoice.

The tradeoff involves settlement speed and volatility management. While card payments offer chargeback protection and fiat stability, stablecoin QR pay 2026 requires users to hold or instantly convert digital assets. However, for businesses prioritizing cost efficiency over dispute mechanisms, the fee disparity is the deciding factor. The industry is shifting toward this model as digital wallets become ubiquitous, reducing the friction of holding stablecoins.

cross border commerce 2026 adoption trends

The architecture of stable qr pay 2026 extends far beyond domestic convenience, addressing the friction of international remittances and cross-border retail. In emerging markets, the primary value proposition is not just speed, but the elimination of the layered fees associated with traditional card networks and correspondent banking. By settling in stablecoins that are instantly redeemable via QR codes, merchants and consumers bypass the 2-3% interchange fees that have long stifled low-value international transactions.

Vietnam and the Philippines serve as the leading testbeds for this interoperability. Both nations have high mobile penetration and significant remittance inflows, making them ideal for testing cross-border QR standards. In Vietnam, the market for QR payments is projected to reach USD 19.81 billion by 2026, with stablecoin-to-QR integration driving a significant portion of this growth (19.1% CAGR). The focus here is on linking local digital wallets with regional payment rails, allowing a tourist from Singapore to pay a vendor in Hanoi using a single QR scan, with settlement occurring instantly in a stable asset.

The Philippines follows a similar trajectory, leveraging its large overseas worker population to drive demand for low-cost, immediate transfers. Here, stable qr pay 2026 functions as a bridge between formal banking systems and informal value transfer systems. Interoperability is the key technical hurdle; successful adoption requires standardized QR formats that work across different national payment switches. When a merchant in Manila accepts a scan from a wallet in Jakarta, the transaction must settle without manual reconciliation, relying on the transparent ledger of the stablecoin network to verify funds in real-time.

This shift transforms cross-border commerce from a back-office banking function into a front-line consumer experience. As interoperability standards mature, the distinction between "domestic" and "international" payments blurs. The result is a unified digital rail where value moves as freely as data, supported by the stability of pegged assets and the ubiquity of QR scanning technology.

No comments yet. Be the first to share your thoughts!