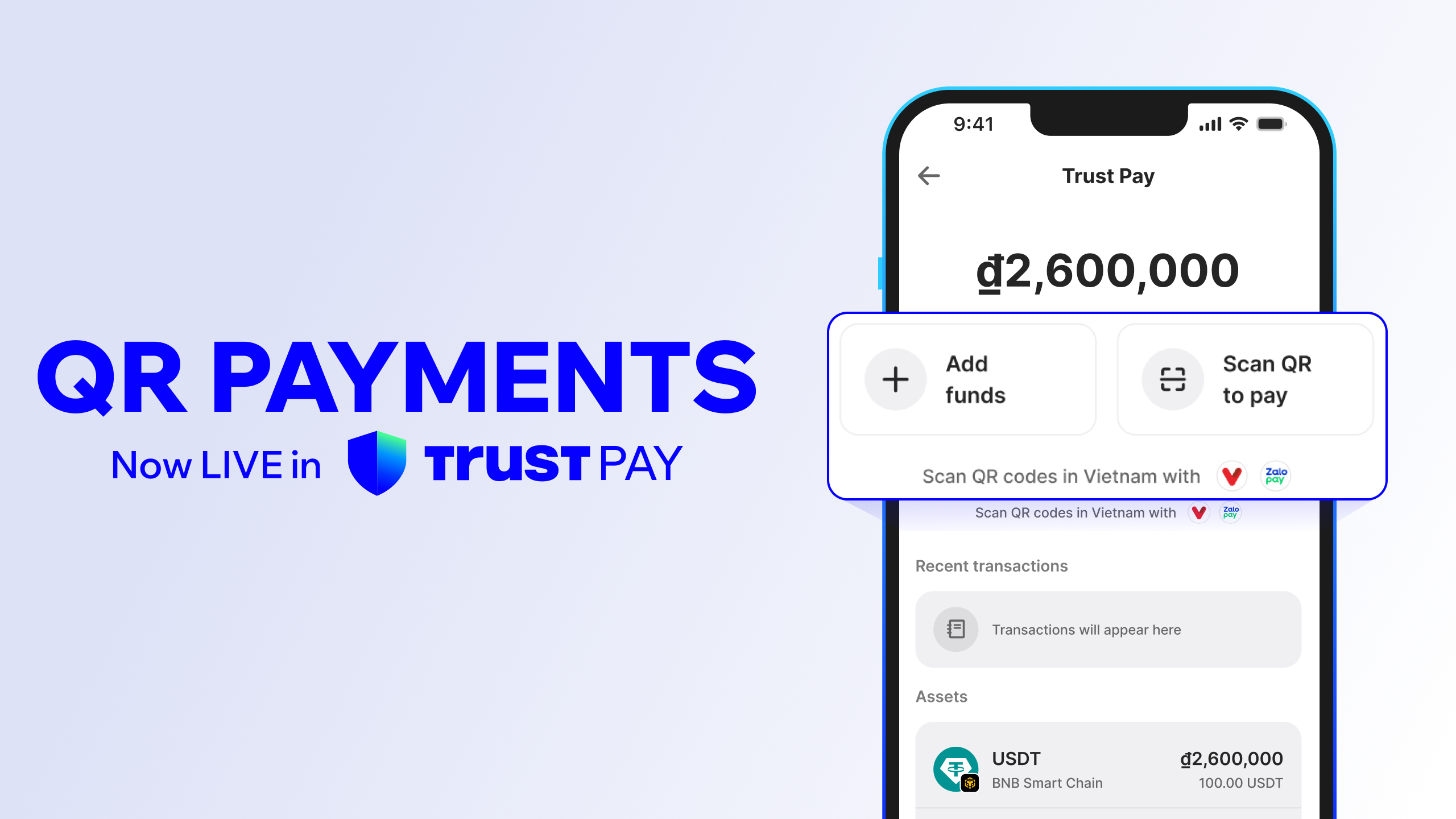

What stable QR pay actually does

Stable QR Pay works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Why merchants prefer instant settlement

Stable QR Pay works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Top stablecoin checkout providers in 2026

Selecting the right infrastructure depends on whether you prioritize self-custody, cross-border flexibility, or local payment network integration. The following platforms represent the leading options for stable QR pay in 2026, each offering distinct advantages for merchants seeking instant fiat settlement.

Trust Wallet provides a self-custodial solution that allows merchants to receive stablecoins and convert them to local currency instantly. This model eliminates the need for third-party custodians, keeping funds under the merchant's control while ensuring immediate liquidity. It is particularly effective for merchants who prefer direct ownership of their digital assets.

Moreta focuses on simplifying cross-border transactions through QR codes. By enabling international travelers to pay merchants abroad without currency exchange friction, Moreta expands the potential customer base for local businesses. This is especially valuable for tourism-heavy regions where foreign visitors frequently use stablecoins.

RedotPay integrates with local payment networks like VietQR, allowing users to pay with stablecoins at any merchant accepting these domestic QR standards. This approach bridges the gap between crypto and traditional banking rails, making stablecoin payments feel familiar to both consumers and merchants.

| Provider | Settlement | Stablecoins | Onboarding | Region |

|---|---|---|---|---|

| Trust Wallet | Instant fiat conversion | USDT, USDC, BNB | Self-custodial wallet setup | Global |

| Moreta | Instant fiat conversion | USDT, USDC | Merchant account creation | Cross-border focus |

| RedotPay | Instant fiat conversion | USDT, USDC | QR code generation via app | Vietnam (via VietQR) |

Security risks and safe scanning practices

Crypto payments offer instant settlement, but the QR code interface introduces a specific vector for fraud known as "quishing." Unlike traditional card numbers that are static, a QR code is a dynamic link. If a merchant is compromised or a scammer overlays a fake code on a legitimate checkout counter, the customer’s stablecoin payment is diverted instantly and irreversibly. In the world of decentralized finance, there is no chargeback mechanism to recover these funds, making verification the only defense.

The primary risk involves phishing sites disguised as payment gateways. When a user scans a malicious QR code, their wallet may connect to a fake interface that mimics a legitimate merchant. The scammer captures the transaction signature or, in worse cases, tricks the user into signing a contract that grants access to their entire wallet balance. This is not a theoretical risk; law enforcement agencies have reported significant losses from QR code scams targeting small businesses and consumers alike.

To mitigate these risks, merchants and customers must adopt a verification-first mindset. Always confirm the destination URL before approving a transaction. For merchants, this means displaying your official, verified QR code in a controlled environment where it cannot be tamperedpered with. Use EMV-compliant standards that link directly to your verified payment processor rather than open-ended crypto addresses.

For those monitoring market volatility while managing security, keeping an eye on stablecoin performance can provide context for transaction timing.

Security in QR payments is not about the technology itself, but about the discipline of the user. By treating every scan as a potential security event, you protect your liquidity from the most common threats in the crypto payment landscape.

Frequently asked questions about stable QR pay

Stable QR pay systems bridge traditional banking rails with blockchain efficiency, offering merchants instant liquidity while keeping transaction costs low. This section addresses the most common concerns regarding security, settlement speed, and technical requirements for 2026 adoption.

Is stable QR pay safer than traditional card payments?

The primary security advantage of stable QR pay is that it eliminates the need to share sensitive card numbers. Instead, transactions are initiated via cryptographic signatures from a digital wallet, significantly reducing the attack surface for data breaches and fraud. To maintain safety, always verify the merchant's QR code visually to prevent "QR code swapping" scams, where fraudsters replace legitimate codes with their own. Using established wallets with built-in transaction previews adds an extra layer of verification before funds are released.

How long does settlement actually take?

Unlike traditional card networks that can take 2-3 business days to settle funds, stable QR payments settle on-chain in seconds. For merchants, this means immediate access to capital, improving cash flow and reducing the need for working capital reserves. While the blockchain confirms the transaction instantly, some payment processors may offer optional fiat conversion, which can introduce a short delay if the merchant prefers holding local currency rather than stablecoins.

What are the typical transaction fees for merchants?

Merchant fees for stable QR pay are generally lower than traditional credit card processing, which often ranges from 1.5% to 3.5%. Stablecoin transactions typically incur network gas fees and a small processor markup, often totaling less than 1%. This cost efficiency is particularly pronounced for cross-border transactions, where traditional wire transfers or card networks charge high foreign exchange and processing fees. The savings compound significantly for high-volume merchants.

Do I need specialized hardware to accept payments?

No specialized hardware is required. Most stable QR pay solutions are software-based, allowing merchants to accept payments using a standard smartphone or tablet. The merchant displays a QR code on their screen or a printed static code, and the customer scans it with their wallet app. For higher-volume environments, integration with existing point-of-sale (POS) systems is available through API connectors from major payment processors, ensuring seamless compatibility with legacy inventory and sales tracking software.

No comments yet. Be the first to share your thoughts!