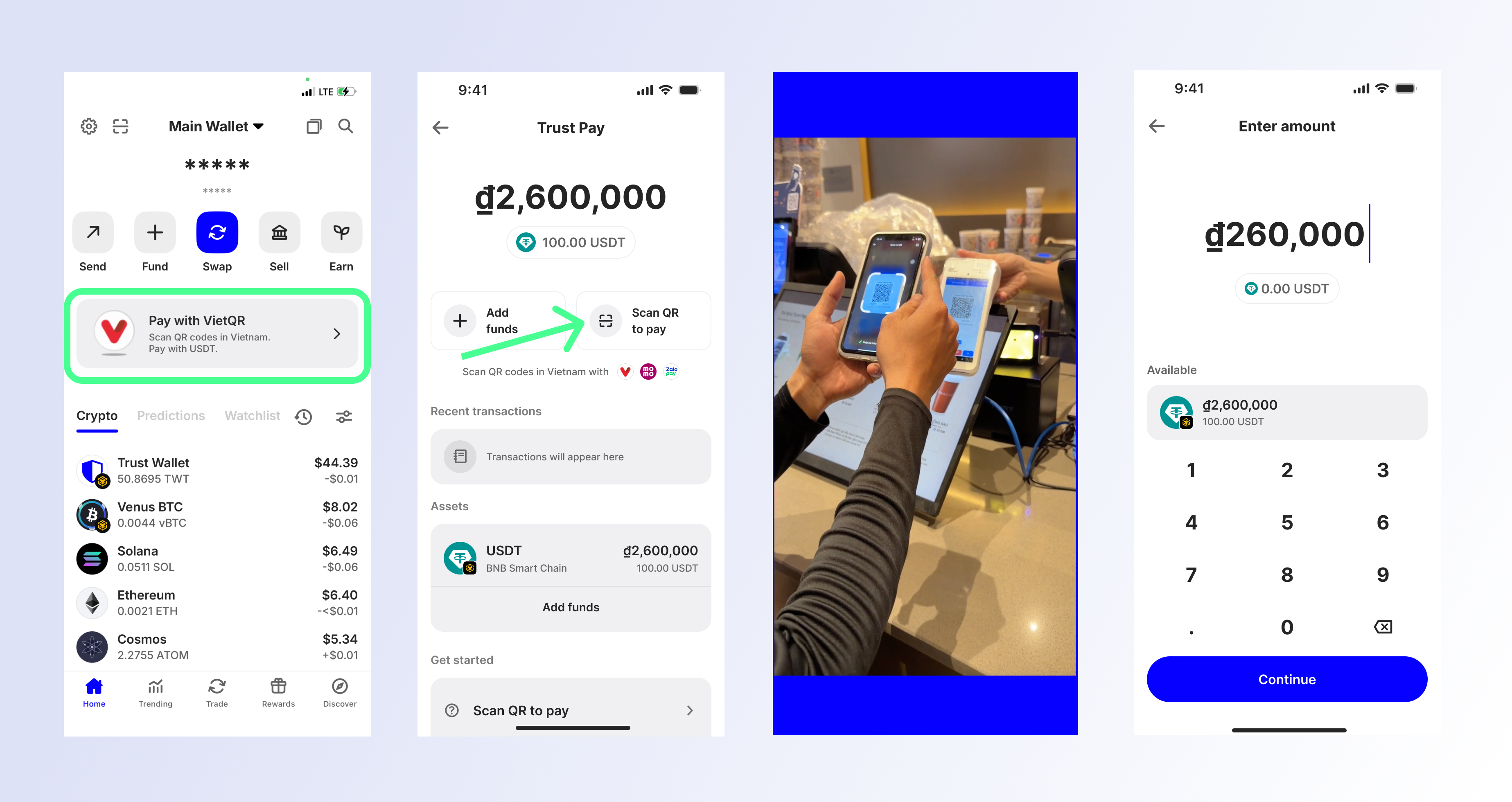

The shift to instant stablecoin settlement

The traditional card network model operates on a T+1 or T+2 settlement cycle, meaning merchants face a multi-day lag between a customer’s purchase and the actual receipt of funds. This delay introduces working capital friction and exposes businesses to chargeback windows that can extend well beyond the initial transaction date. Stablecoin QR payments disrupt this timeline by offering instant, final settlement. When a customer scans a QR code to pay in a stablecoin like USDT or USDC, the blockchain confirms the transaction in seconds, and the funds are immediately available in the merchant’s wallet.

This immediacy is not merely a speed advantage; it is a risk mitigation tool. By bypassing the card association’s clearinghouse, merchants eliminate the possibility of post-transaction disputes reversing settled funds—a common vulnerability in card-based retail. The operational reality is a shift from "pending" balances to confirmed cash flow. For high-volume retail environments, this reduces the need for float capital and simplifies reconciliation processes that previously required complex accounting layers to match delayed bank deposits with point-of-sale records.

The predictability of this settlement is anchored in the stability of the underlying asset. Unlike volatile cryptocurrencies, stablecoins are pegged to fiat currencies, ensuring that the value received at the moment of scan is the value settled. This stability is critical for merchants who cannot absorb currency fluctuation risk during the settlement window. The following chart illustrates the price stability of major stablecoins over recent periods, demonstrating the low volatility that makes them viable for daily retail operations.

Comparing stable QR pay providers

Selecting an infrastructure partner for stablecoin QR payments requires evaluating three operational metrics: fee structure, supported blockchain networks, and settlement latency. For merchants prioritizing instant settlement, the choice between custodial and non-custodial rails determines both risk exposure and customer experience.

The table below contrasts the core capabilities of four primary providers. Data reflects standard merchant-tier configurations as of early 2026.

| Provider | Merchant Fees | Supported Chains | Settlement Speed |

|---|---|---|---|

| Cobo | 0.5-1.0% | Multi-chain (ETH, BSC, Polygon) | Instant (on-chain) |

| Stripe Crypto | 1.5% | ETH, Polygon, Base | Instant (fiat conversion) |

| Circle | Variable (API) | USDC-native (Multi-chain) | Instant (USDC) |

| Fireblocks | Custom (Enterprise) | Multi-chain (Institutional) | Instant (vault-to-vault) |

Fee Structures and Margins Stripe Crypto charges a flat 1.5% fee, which includes automatic conversion to fiat. This simplifies accounting but reduces margins for high-volume merchants. Cobo and Fireblocks offer lower base fees (0.5-1.0% or custom enterprise rates) but require merchants to manage stablecoin exposure or integrate their own liquidity providers. Circle’s API pricing is variable, often scaling with transaction volume, making it suitable for large-scale operations.

Chain Support and Liquidity Multi-chain support is critical for QR payments, as customers may hold stablecoins on Ethereum, Polygon, or BSC. Cobo and Fireblocks support the widest range of networks, reducing friction for users on Layer 2 chains. Stripe and Circle focus on major L2s (Polygon, Base) to balance speed and cost. Merchants should verify that their chosen provider supports the specific stablecoin (USDC, USDT) and chain their customer base predominantly uses.

Settlement Latency "Instant" in stablecoin payments means on-chain confirmation, typically 2-5 seconds on L2s. Stripe’s "instant" settlement refers to fiat availability, which may involve a brief holding period for fraud checks. Cobo and Circle provide immediate stablecoin receipt in merchant wallets, allowing for immediate reconciliation. For offline retail, where network reliability varies, providers with robust fallback mechanisms for chain congestion are preferred.

Integrating crypto into legacy POS

Bridging existing point-of-sale hardware with stablecoin settlement requires a layered technical approach rather than a full system replacement. In 2026, the operational reality for merchants is defined by middleware that translates traditional tender signals into blockchain transactions. This architecture allows legacy terminals to process QR-based payments without altering the core ledger or requiring immediate hardware upgrades.

The integration follows a precise sequence to ensure instant settlement and regulatory compliance.

Merchants install a specialized payment gateway that acts as the bridge between their existing POS and the blockchain network. This software layer handles the generation of unique, dynamic QR codes for each transaction. The gateway manages the cryptographic signing of the payment request, ensuring that the stablecoin transfer is initiated securely from the customer’s wallet to the merchant’s designated address.

Unlike traditional card networks that settle in T+1 or T+2, stablecoin integrations are configured for near-instant finality. The gateway connects to liquidity providers or stablecoin issuers to facilitate immediate conversion to fiat or retention in stable assets. This step requires careful configuration of wallet addresses and multi-signature requirements to prevent fraud and ensure that funds are cleared before the receipt is printed.

The final step involves mapping the blockchain transaction hash back to the merchant’s internal accounting system. The gateway sends a confirmation signal to the legacy POS once the blockchain confirms the block. This synchronization updates the sales ledger in real-time, allowing the merchant to reconcile digital sales alongside cash and card transactions without manual intervention or delayed batch processing.

This middleware approach minimizes downtime and capital expenditure. However, it introduces a dependency on network stability and gateway uptime. Merchants must monitor the health of the integration layer to ensure that the promise of instant settlement is not compromised by technical latency or connectivity issues during peak hours.

When QR beats NFC for merchants

While NFC tap-to-pay offers speed, QR codes with stablecoin settlement provide superior economics for cross-border and low-margin retail. The trade-off is operational friction: scanning a code takes longer than tapping a card, but it bypasses the traditional card network's interchange fees and settlement delays.

For merchants operating in developing markets or handling international transactions, the cost differential is decisive. Traditional card payments often incur 2-3% in interchange fees plus currency conversion spreads. QR-based stablecoin payments can reduce this to near-zero network fees, settling instantly on-chain. This efficiency matters most for small-ticket items where card fees erode thin margins.

The choice hinges on transaction volume and geography. NFC remains the gold standard for domestic, high-frequency retail where speed drives throughput. However, for merchants facing high cross-border fees or slow traditional settlement cycles, QR codes offer a pragmatic, cost-effective alternative with instant finality.

Merchant checklist for adoption

Launching stable QR pay requires rigorous pre-flight verification. Unlike traditional card networks, stablecoin settlement relies on blockchain finality, meaning errors are irreversible and technical readiness is non-negotiable. Before going live, merchants must validate their infrastructure against the following operational realities.

- Payment Gateway Compatibility: Verify that your POS or gateway provider supports the specific stablecoin standard (e.g., ERC-20, BEP-20) and network you intend to use. Ensure the provider offers instant fiat conversion or stablecoin settlement options, as this is the primary differentiator for cash flow management.

- Network Fee Structure: Calculate the impact of gas fees on small-ticket transactions. If your average order value is low, consider aggregating settlements or using Layer-2 solutions to maintain margin integrity. High transaction fees can erode the cost advantages of crypto-payments.

- Regulatory Compliance & KYC: Confirm that your provider adheres to local anti-money laundering (AML) and know-your-customer (KYC) regulations. In many jurisdictions, merchants must report transactions above certain thresholds or maintain audit trails for blockchain transfers.

- Customer Onboarding Flow: Test the end-to-end user experience. Customers must have a compatible wallet and sufficient stablecoin balance. Friction in the scanning process can lead to abandoned carts, especially in high-volume retail environments.

- Reconciliation & Accounting: Integrate blockchain data with your existing accounting software. Automated reconciliation is essential to match on-chain settlement hashes with internal sales records, ensuring accurate financial reporting.

Failure to address these points can result in settlement delays, compliance penalties, or operational bottlenecks. Treat this checklist as a mandatory audit before accepting any digital asset payments.

Common questions about stable QR pay

Stable QR payments represent a structural shift in retail settlement, but operational realities differ from marketing claims. The following addresses specific friction points merchants and consumers face when adopting this technology.

Settlement speed and risk

Unlike traditional card networks that rely on multi-day clearing cycles, stable QR payments aim for near-instant settlement. This reduces counterparty risk for merchants but requires robust liquidity management. Merchants must ensure their wallets can absorb volatility if the stablecoin peg deviates, even slightly.

No comments yet. Be the first to share your thoughts!