Why stable QR pay matters now

Stablecoin QR payments solve the two biggest friction points for merchants: settlement delay and processing cost. Unlike traditional card networks that hold funds for days, stablecoin QR transactions settle in seconds on-chain, giving you immediate access to capital. This speed transforms cash flow management, especially for high-volume or cross-border operations.

The economic advantage is stark. Traditional payment rails often charge 2-3% per transaction, plus fixed fees. Stablecoin QR payments typically cost a fraction of that, often less than 1%. When you combine near-zero fees with instant settlement, the margin improvement is significant. For a merchant processing $100,000 monthly, these savings can add up to thousands of dollars annually.

Adoption is accelerating because the infrastructure is now reliable. In 2026, over 100 million Americans use smartphone QR scanners regularly, making the customer experience seamless. You no longer need expensive hardware; a simple smartphone camera is enough to receive payments. The QR Code payment market is projected to grow from $18.6 billion in 2026 to $85.7 billion by 2036, signaling a permanent shift in how commerce is conducted.

While security depends on the platform you choose, the underlying technology is mature. Stablecoins now transact over USD 1 trillion daily, surpassing Visa and Mastercard combined volumes. This scale proves that the network can handle merchant-level demand without congestion or failure. By adopting stable QR pay, you are not just cutting costs; you are future-proofing your checkout process against the rising fees and delays of legacy banking systems.

Choose your stablecoin payment provider

Selecting a payment processor is the most critical decision for setting up stablecoin QR payments. You need a provider that handles the blockchain complexity while presenting a familiar checkout experience to your customers. The goal is to accept USDC or USDT, convert it if necessary, and settle in your local currency with minimal friction and clear compliance.

Start by verifying which stablecoins the processor supports. Not all providers accept USDT, and some only support USDC on specific networks like Solana or Polygon. Ensure the provider offers a native QR code scanning interface or integrates seamlessly with your existing POS system. This step ensures your customers can pay with a simple scan rather than navigating complex wallet addresses.

Next, compare the fee structures. Traditional card processors charge interchange fees plus a percentage. Stablecoin processors typically charge a flat fee or a lower percentage, but you must account for network gas fees and any conversion costs if you choose to settle in fiat. Look for providers that offer transparent pricing without hidden withdrawal fees.

| Provider | Chains | Settlement | QR Setup |

|---|---|---|---|

Ensure the provider is registered with relevant financial authorities in your jurisdiction. This is non-negotiable for high-stakes merchant accounts. Check if they offer KYC/AML tools for your business verification process.

Run a test transaction using a real customer wallet. Verify that the QR code generates instantly, the payment confirms on-chain, and your dashboard updates in real-time. Pay attention to the time it takes for the funds to appear in your settlement account.

Connect the provider’s API to your point-of-sale system. Most providers offer plugins for major platforms like Shopify or WooCommerce, or a custom API for bespoke systems. Ensure the receipt generation includes a blockchain transaction hash for record-keeping.

Install the QR payment widget

Adding the QR payment widget to your existing POS or checkout flow bridges the gap between your current interface and on-chain settlement. The widget handles the cryptographic signing and transaction broadcasting, allowing your system to focus on order management rather than blockchain mechanics. By embedding this component, you enable customers to scan a code with their mobile wallet and pay in seconds using stablecoins like USDC.

The integration follows a standard sequence: you initialize the widget, configure the payment parameters, and render the QR code for the customer. Once the customer scans the code and confirms the transaction in their wallet, the widget detects the on-chain confirmation and triggers your success callback. This ensures your inventory and accounting systems update only after the funds are settled.

1. Initialize the SDK

Begin by installing the official stablecoin payment SDK into your project. This package provides the necessary functions to generate secure QR payloads and listen for transaction events. Import the core module and instantiate the client using your merchant API keys. Ensure your environment variables are configured to point to the production network, not the testnet, before proceeding.

2. Configure Payment Parameters

Define the transaction details that the widget will display. This includes the currency (e.g., USDC), the exact amount, and the recipient wallet address. The widget validates these parameters against the blockchain’s current state to prevent display errors. You can also set optional fields like a memo or reference ID to help reconcile the payment with your internal order system later.

3. Render the QR Code

Call the render method to display the QR code in your checkout UI. The widget generates a dynamic URI that encodes the payment request. Customers use their smartphone wallets to scan this code. The visual output should be high-contrast and large enough to be scanned easily in low-light environments. The widget automatically handles the expiration of the QR code if the customer does not pay within the specified time window.

4. Handle Transaction Events

Attach event listeners to the widget to monitor the payment lifecycle. You will receive callbacks for payment_initiated, payment_pending, and payment_confirmed. Use the payment_confirmed event to update your order status to "Paid." If the transaction fails or is rejected by the user, handle the payment_failed event to inform the customer and offer retry options. This real-time feedback loop is critical for maintaining a smooth checkout experience.

5. Verify On-Chain Settlement

While the widget provides immediate feedback, always perform a final verification on the blockchain. Check the transaction hash returned by the widget against a block explorer to ensure the funds have reached your wallet. This step protects against potential double-spending attempts or network reorgs, ensuring that your revenue is secure before you fulfill the order.

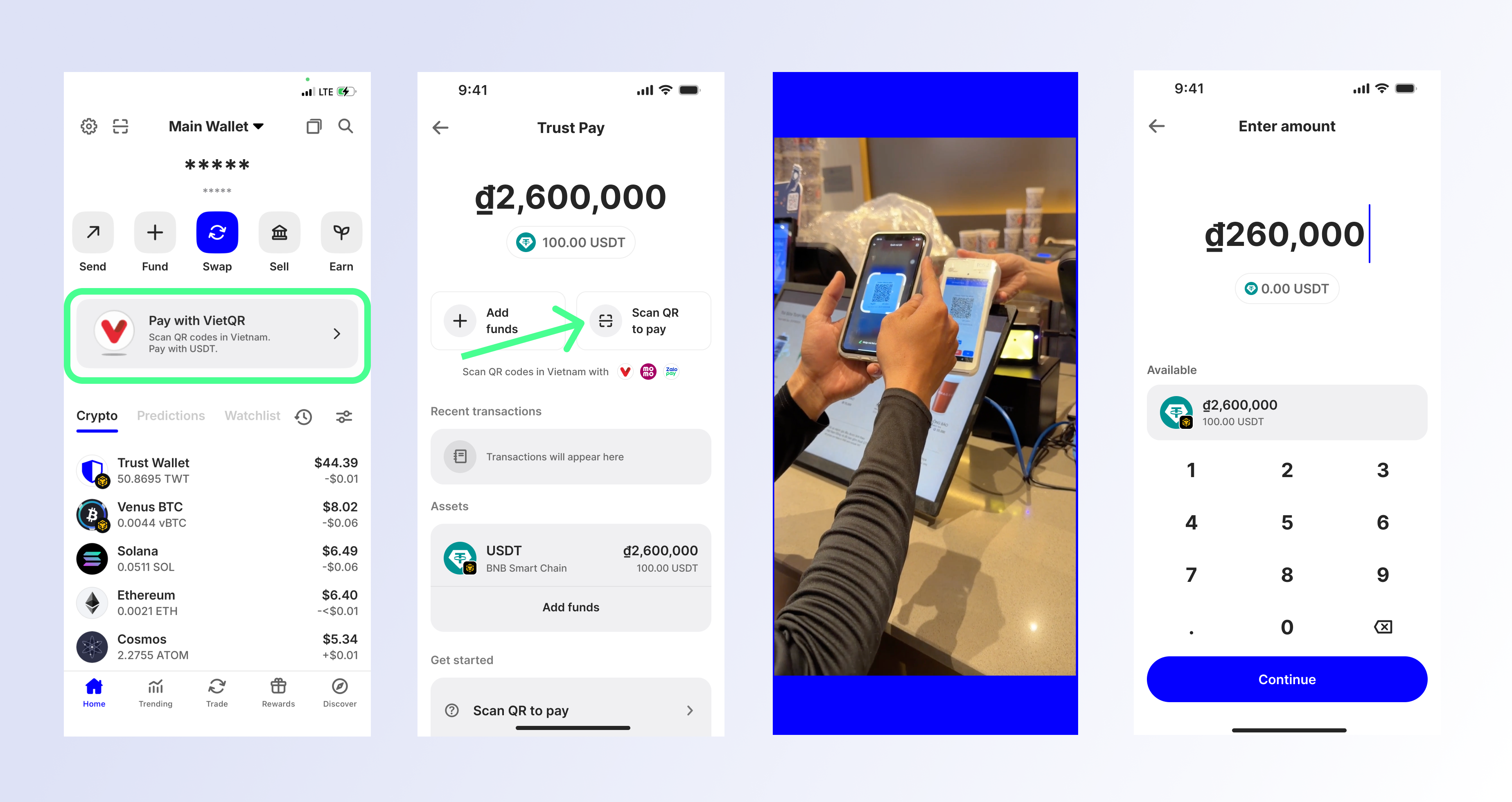

Configure instant settlement rules

To achieve instant stablecoin settlement, you must configure your payment gateway’s backend to handle the conversion or holding of digital assets before they reach the merchant’s bank account. This setup bridges the gap between the blockchain and traditional banking, ensuring that funds are available immediately after a customer scans a QR code.

1. Select your settlement model

You generally have two options for how stablecoins are handled after the transaction is confirmed on-chain:

- Auto-Conversion (Fiat Settlement): The payment processor automatically converts the received stablecoin (e.g., USDC or USDT) into fiat currency (USD, EUR) and deposits it into your bank account. This is the most common method for merchants who want to avoid crypto volatility and accounting complexity.

- Stablecoin Holding: The merchant chooses to keep the funds in stablecoins. This requires a crypto-friendly custodian or wallet solution and is suitable for businesses that want to retain exposure to digital assets or use them for cross-border payments.

2. Link and verify your bank account

For auto-conversion to work, your business bank account must be linked and verified within the payment gateway’s dashboard. Ensure the account is in good standing and matches the legal entity registered with the processor. Most gateways use micro-deposit verification or API-based bank linking (such as Plaid) to confirm ownership instantly.

3. Set fee thresholds and payout schedules

Configure the minimum transaction amount that triggers an immediate payout. You can also set daily or weekly payout limits to manage cash flow and mitigate fraud risk. While "instant" settlement is possible, most gateways process payouts in batches during banking hours to comply with AML (Anti-Money Laundering) regulations.

4. Test with a small transaction

Before going live, run a test transaction of $1.00. Verify that the stablecoin is received, the conversion (if applicable) occurs, and the fiat funds appear in your bank account within the expected timeframe (usually minutes to a few hours). Check your dashboard for accurate transaction records and fee deductions.

Link your existing payment gateway or QR code provider to your merchant dashboard. This establishes the channel through which stablecoin transactions will be routed.

Input and verify your business bank account information. Use micro-deposit verification or API linking to ensure the account is active and belongs to your business entity.

Decide whether to auto-convert stablecoins to fiat or hold them. Set your preferred settlement currency and configure any minimum payout thresholds.

Process a small test payment (e.g., $1.00) to confirm that funds move correctly from the customer’s wallet to your bank account or crypto wallet.

Test the payment flow end-to-end

Before going live, run a full transaction cycle to verify that your QR code generates correctly, the customer’s wallet signs the transaction, and the funds settle in your merchant account. This validation prevents costly errors during peak hours.

Open your POS system or payment gateway and create a test QR code for a small amount, such as $1.00 in USDC. Ensure the code encodes the correct wallet address and currency. Scan it with a consumer wallet to confirm it resolves to the right destination.

Use a separate test wallet to scan the generated QR code. Initiate the payment and sign the transaction. Watch for the confirmation screen in the customer wallet, which indicates the blockchain has processed the request. This step verifies the signing process works as expected.

Log into your merchant dashboard or check your receiving wallet. Confirm that the stablecoin amount has appeared and is ready for withdrawal or conversion. Check that the transaction hash is recorded in your sales logs. If the funds do not appear within the expected block time, check your network settings.

If the QR code fails to scan, verify that your encoding format matches the standard used by major wallets (e.g., BEP-20, ERC-20). If the transaction hangs, ensure your merchant wallet is on the correct blockchain network. Testing these scenarios offline ensures a smooth experience for your customers when you accept Stable QR Pay live.

Common stable QR pay mistakes

Even with instant settlement, small errors can drain margins or halt sales. Treat your setup like a cash register: if the drawer isn’t aligned, the money doesn’t land where it should. Below are the most frequent pitfalls merchants face when adopting stable QR payments, along with the fixes that keep transactions clean.

Ignoring network fees

Stablecoins move on blockchains, not banks. While USDC or USDT transfers are cheap, they are not free. Ethereum mainnet fees can spike during congestion, eating into thin retail margins. If you accept payments on a high-fee chain without a fee-shifting mechanism or a Layer-2 alternative, your profit margin shrinks with every transaction. Check the current gas rates for your chosen network before going live. Juniper Research notes that QR payments are surging, but volume doesn’t offset poor cost management.

Failing to verify the recipient address

QR codes are static images; they don’t encrypt data. A malicious actor can swap a printed QR code at your checkout counter with one pointing to their wallet. Stripe warns that QR codes themselves lack built-in security layers. Always verify the destination address on your merchant dashboard matches the code displayed. If you use dynamic QR codes that generate a unique address per transaction, this risk drops significantly.

Using the wrong stablecoin

Not all stablecoins are created equal. Some have lower liquidity or higher volatility against the fiat currency you rely on for payroll. If your supplier expects USD, accepting a stablecoin pegged loosely to the dollar introduces exchange risk. Stick to widely adopted assets like USDC or USDT on networks with deep liquidity. Ensure your payment processor supports immediate fiat conversion if you don’t want to hold crypto on your books.

Skipping the test transaction

Never go live without sending a test payment. A $1.00 test confirms that the QR code scans correctly, the network processes the transaction, and the funds hit your wallet. It also reveals if your merchant account is properly linked to the correct blockchain network. A mismatched network (e.g., sending ERC-20 USDC to an TRC-20 address) results in lost funds.

Not having a backup payment method

Networks go down. Power outages happen. If your QR pay system is your only option, you lose sales the moment technology fails. Always keep a card terminal or cash option ready. This isn’t about doubting the technology; it’s about business continuity. Customers appreciate flexibility, and you’ll avoid angry customers standing at the register with no way to pay.

Frequently asked questions about stable QR pay

Are QR codes still relevant in 2026?

Yes. QR codes remain a primary payment method. In 2026, over 100 million Americans are expected to use smartphone QR scanners. The QR code market is projected to reach $33.14 billion by 2031. For merchants, this means QR is no longer an experimental tool but a standard operational component for instant stablecoin settlement.

What is the disadvantage of QR code payments?

The main drawback is security risk. The QR code itself contains no security measures. Security depends entirely on the app or platform processing the transaction. Merchants must rely on trusted payment gateways to handle encryption and fraud prevention, rather than the code structure itself.

Is stable QR pay better than credit cards?

Stable QR payments offer faster settlement than credit cards. Credit card transactions often take days to clear, while stablecoin QR payments settle instantly on-chain. This reduces cash flow delays for merchants and eliminates chargeback risks associated with traditional card networks.

No comments yet. Be the first to share your thoughts!