Stable QR payments 2026: Limits and Provider Selection

Use this section to compare QR payment options in real life, separating must-have requirements from nice-to-have features. A practical choice should survive normal use, maintenance, timing, and budget constraints. If a recommendation only works in an ideal situation, call that out plainly and provide a fallback path.

The simplest way to evaluate options is to write down must-have criteria first, then compare each provider against those criteria before weighing secondary features.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

How to Choose a Stablecoin QR Pay Provider

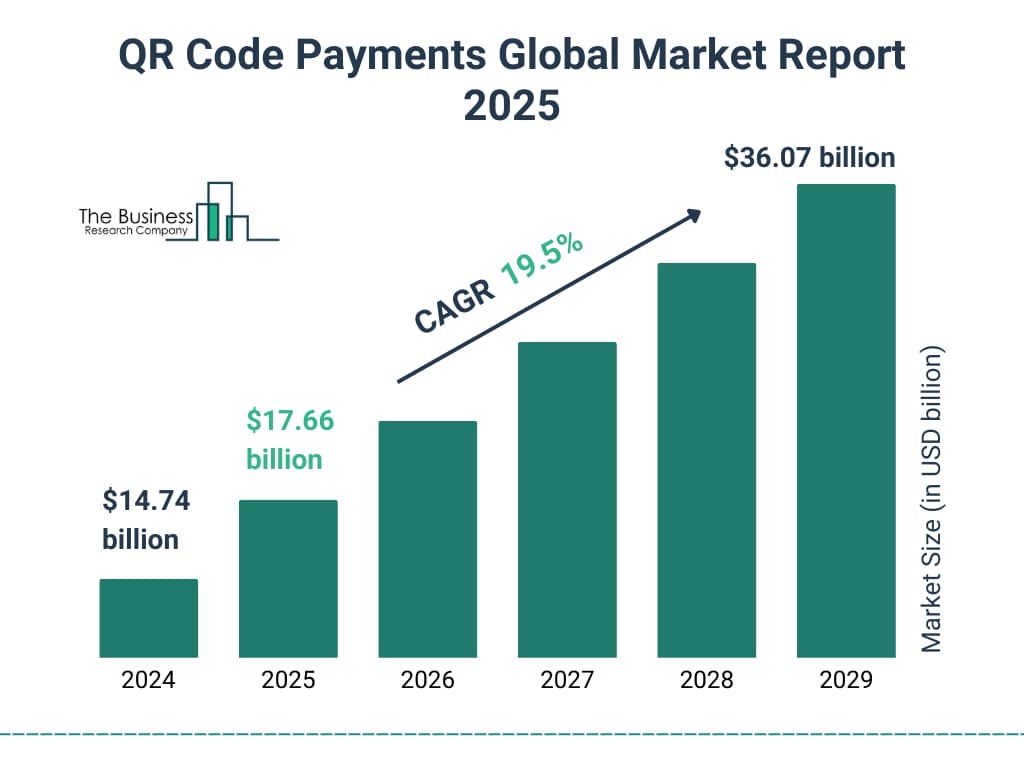

Selecting a payment rail for your SMB requires matching your volume, risk tolerance, and settlement needs. Juniper Research projects QR code payments will grow 50% globally from $5.4 trillion in 2025, meaning the infrastructure you choose today will define your operational baseline for years. Use this framework to evaluate providers based on five critical factors.

Traditional QR systems often batch settlements, holding funds for T+1 or T+2 days. Stablecoin-integrated QR payments offer near-instant finality. Choose a provider that settles directly to your digital wallet rather than routing through a third-party merchant account. This reduces counterparty risk and improves cash flow for daily operations.

Not all stablecoins are created equal. Prioritize providers using fully reserved, fiat-backed stablecoins like USDC or USDT that comply with local financial regulations. If you operate in multiple regions, ensure the provider supports the specific stablecoin variants accepted in each jurisdiction. Avoid providers that rely on algorithmic or unbacked tokens, as these introduce unnecessary volatility and regulatory uncertainty.

High-volume SMBs need to know if the provider supports large transactions without friction. While traditional UPI QR codes in markets like India have raised limits to Rs. 2 lakh, stablecoin QR systems often scale more flexibly. Compare the provider’s fee structure: look for flat fees or low percentage rates that do not spike during high-volume periods. Ensure the provider’s limit aligns with your average ticket size to avoid declined sales.

The best technology fails if customers find it confusing. Choose a provider whose QR code works seamlessly with popular consumer wallets and doesn’t require customers to download a new app. The scan-to-pay flow should take less than three seconds. If your staff uses POS systems, ensure the provider offers a direct API integration that automatically reconciles stablecoin transactions with your accounting software.

Stablecoin transactions are irreversible. A reliable provider must offer robust customer support and clear dispute resolution protocols for errors, such as incorrect addresses or double-scans. Look for providers that offer 24/7 support and have a transparent process for handling failed transactions. This safety net is critical for maintaining customer trust and protecting your revenue.

Spotting Weak QR Pay Claims

Stablecoin integration sounds like a silver bullet for SMB settlement times, but the marketing often outpaces the infrastructure. Before committing to a new QR pay provider, SMBs need to separate the underlying network speed from the actual settlement reality. Many vendors advertise "instant" payments while their fiat on-ramps still rely on batch processing that delays liquidity by T+1 or worse. Check the provider’s settlement schedule explicitly. If the whitepaper mentions "T+0" but the FAQ lists 24-hour windows for large volumes, the claim is misleading.

Another common trap is assuming QR codes are just a consumer-facing gimmick. While they are familiar and device-agnostic, their real value in 2026 lies in their role as a universal access layer for structured data. A scan should trigger more than a payment; it should surface origin, materials, and safety documentation. If a provider’s QR solution only handles basic transaction routing without supporting rich metadata or cross-border stablecoin rails, it’s a weak option for businesses looking to scale globally.

Finally, be wary of transaction limit claims that ignore regulatory caps. While some regions like India have raised UPI limits to ₹2 lakh, stablecoin QR payments operate under different compliance frameworks. Ensure the provider clearly outlines daily and per-transaction limits for stablecoin settlements. Without transparent limits, an SMB might face frozen funds during peak periods, defeating the purpose of instant settlements. Always verify the provider’s compliance with local anti-money laundering (AML) rules before integrating.

Stable QR payments 2026: What to check next

Stablecoin integration is shifting QR payments from simple convenience to a high-volume financial rail. SMBs need to understand the practical limits and current market position before adopting these systems.

No comments yet. Be the first to share your thoughts!