Stable qr pay 2026 limits to account for

How Stable QR Pay is Redefining Instant Settlements works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Stable qr pay 2026 choices that change the plan

Adopting stablecoin QR payments in 2026 requires balancing speed against infrastructure readiness. While the technology promises near-instant settlement, the reality on the ground involves distinct operational tradeoffs that merchants must weigh before upgrading their point-of-sale systems.

Network volatility and finality

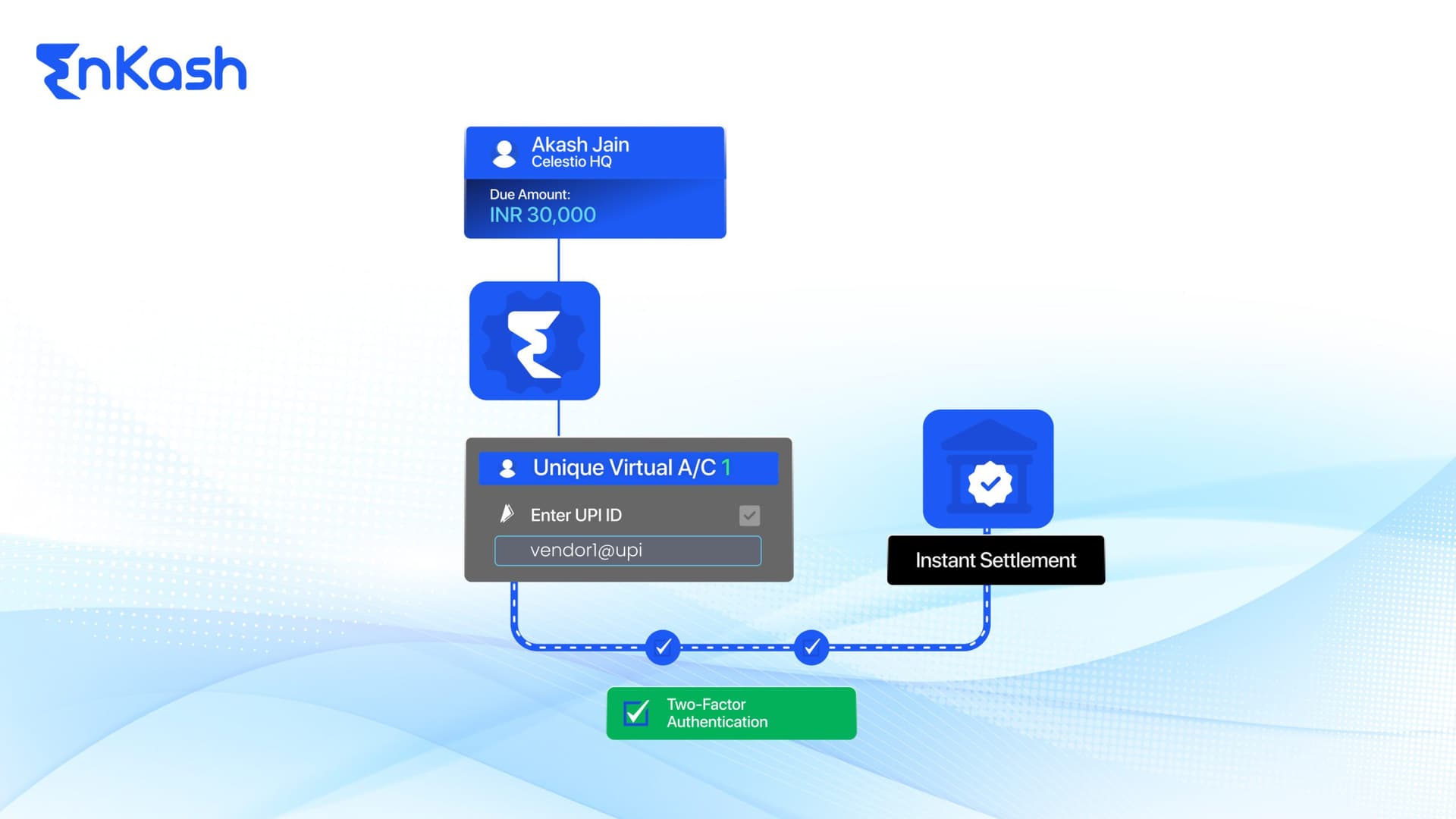

Stablecoins are pegged to fiat currencies, but they still settle on blockchains that can experience congestion. During peak hours, transaction fees may spike, and finality can take seconds rather than milliseconds. Unlike traditional card networks, which guarantee a chargeback window, blockchain settlements are often irreversible. Merchants must decide if they can absorb the risk of erroneous payments or if they need a third-party processor to act as a buffer.

Merchant hardware compatibility

Most modern point-of-sale (POS) systems in 2026 support QR-based cashless payments, but legacy hardware may require upgrades. Some systems need specific software patches to recognize stablecoin QR standards, while others rely on external mobile scanners. Before committing, audit your current terminals to ensure they can process the specific stablecoin protocols your customers prefer. This avoids the friction of abandoned carts at checkout.

Regulatory and tax clarity

Tax treatment of stablecoin transactions varies by jurisdiction. In some regions, every scan is considered a taxable event, requiring detailed record-keeping for each micro-transaction. Others treat stablecoins as property, complicating accounting. Merchants should consult local tax authorities to understand if they need specialized software to track these flows. Failure to comply can lead to audits or penalties that outweigh the benefits of faster settlement.

Customer adoption and friction

While QR codes remain a familiar interface, the underlying asset must be accessible to the average consumer. If your customers do not already hold stablecoins in a digital wallet, the friction of onboarding may outweigh the convenience of the scan. Merchants in high-traffic, low-margin environments may find that the learning curve for customers reduces transaction volume initially. It is a balance between technological innovation and customer ease.

| Tradeoff Factor | Benefit | Risk / Drawback |

|---|---|---|

| Settlement Speed | Near-instant finality | Blockchain congestion delays |

| Transaction Cost | Lower fees than card networks | Variable gas fees during peaks |

| Chargebacks | Irreversible payments protect revenue | No buyer protection may reduce trust |

| Integration | Standard QR interface | Legacy POS hardware may need updates |

Choose the next step

How Stable QR Pay is Redefining Instant Settlements works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The Quiet Traps in Stable QR Payments

Stablecoin QR payments promise instant settlement, but the infrastructure beneath the scan is fragile. Merchants often overlook the gap between the user interface and the blockchain reality. The code is just a launcher; the settlement layer is where the risk lives.

Hidden Gas Volatility

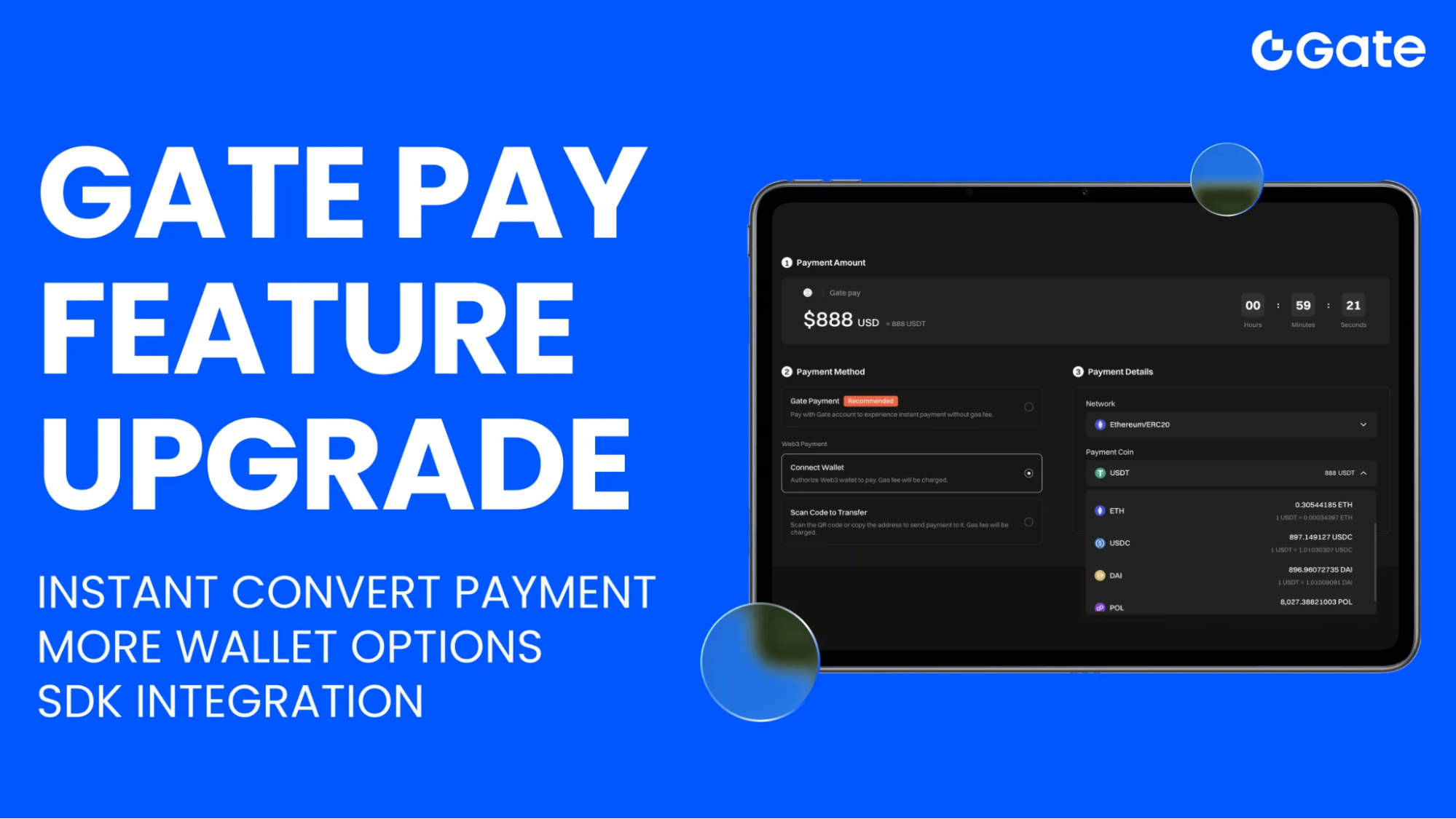

A QR code may display a stable amount, but the underlying transaction requires gas. If the network is congested, the merchant might receive less than expected after fees are deducted from the principal. Always verify if the payment gateway absorbs gas costs or passes them to the buyer. Unchecked, these micro-fees erode margins on small transactions.

Provider Sunset Risks

Not all QR payment providers are built for longevity. Some platforms act as temporary bridges, discontinuing services abruptly due to regulatory pressure or technical debt. For example, Trust Wallet recently announced the temporary discontinuation of its QR payment feature due to provider changes. Relying on a single provider without an exit strategy leaves your checkout flow vulnerable to sudden outages.

Regulatory Ambiguity

Stablecoins exist in a gray area of financial regulation. While QR codes themselves are widely used as an access layer because they are device-agnostic, the funds they move may not be insured. In regions like India, UPI QR codes have high transaction limits (up to Rs. 2 lakh), but stablecoin QR equivalents often lack similar consumer protections. Merchants must assume their funds are exposed to smart contract risks and regulatory crackdowns.

Vendor Lock-in

Many QR payment solutions are proprietary. Switching providers often means migrating customer data and reconfiguring POS systems. This friction discourages competition, allowing vendors to raise fees over time. Choose open-standard protocols where possible to maintain flexibility. The convenience of a single-scan payment shouldn't come at the cost of long-term operational control.

No comments yet. Be the first to share your thoughts!