Why stablecoin payments 2026 matter for merchants

The operational mechanics of merchant settlement are undergoing a structural shift. In 2026, the primary value proposition of stablecoin payments is no longer theoretical speculation but an established utility focused on settlement finality and cost reduction. Traditional banking rails, which often rely on correspondent networks and legacy clearinghouses, introduce latency and friction that erode merchant margins. Stablecoins bypass these intermediaries, allowing funds to move directly from payer to payee on-chain.

Fee structures represent the second critical driver for adoption. According to data from BVNK’s 2026 Utility Report, lower transaction fees are the leading factor driving stablecoin adoption among users, cited by 30% of respondents. This contrasts sharply with traditional credit card networks, where merchant discount rates can range from 1.5% to 3.5% plus fixed per-transaction fees. Stablecoin networks, particularly those optimized for payments like Solana or Polygon, offer transaction costs that are fractions of a cent, preserving margin for low-ticket items and high-volume e-commerce.

Stripe’s analysis of 2026 business trends highlights that stablecoins also reduce foreign exchange (FX) markups. In cross-border scenarios, traditional banks often apply significant spreads on currency conversion. Stablecoins, primarily pegged to the US dollar, allow merchants to receive payment in a stable asset without the layered currency conversion costs inherent in SWIFT transfers. This transparency in pricing and speed makes stablecoin payments a competitive necessity rather than a niche experiment for international merchants.

Regulatory clarity drives enterprise adoption

The passage of the Genius Act in July 2025 marked a structural shift in the stablecoin ecosystem, transitioning digital assets from a speculative frontier to a regulated utility. By establishing a clear federal framework for payment stablecoins, the legislation addressed the primary compliance barrier that had previously deterred traditional merchants and financial institutions from adopting blockchain-based settlement layers. This regulatory certainty has effectively de-risked the technology, allowing businesses to integrate stablecoin payments with the same confidence they apply to traditional wire transfers or card networks.

The core value proposition for merchants lies in the combination of regulatory compliance and operational efficiency. Unlike decentralized cryptocurrencies, payment stablecoins under the new framework are subject to strict reserve requirements and oversight, ensuring that the digital token is fully backed by liquid, high-quality assets. This alignment with existing financial regulations means that merchants no longer need to navigate ambiguous legal landscapes or maintain separate compliance teams for digital asset handling. Instead, they can leverage the speed of blockchain settlement while remaining firmly within the bounds of federal law.

Official analysis from the Federal Reserve highlights the implications of this shift, particularly regarding cross-border payments and monetary policy. The integration of regulated stablecoins into the mainstream financial infrastructure promises to reduce settlement times from days to seconds, significantly improving cash flow for businesses engaged in international trade. By removing the friction of intermediary banks and reducing the cost of compliance, the new regulatory environment positions stablecoins as a viable alternative for high-volume, low-margin transactions.

As major payment processors and financial institutions begin to build infrastructure around this new framework, the adoption curve is expected to accelerate. The focus has shifted from technological experimentation to practical integration, with an emphasis on settlement finality and auditability. For merchants, this means that stablecoin payments are no longer a niche option but a standard, compliant method for receiving payments, backed by the same regulatory rigor that protects traditional banking transactions.

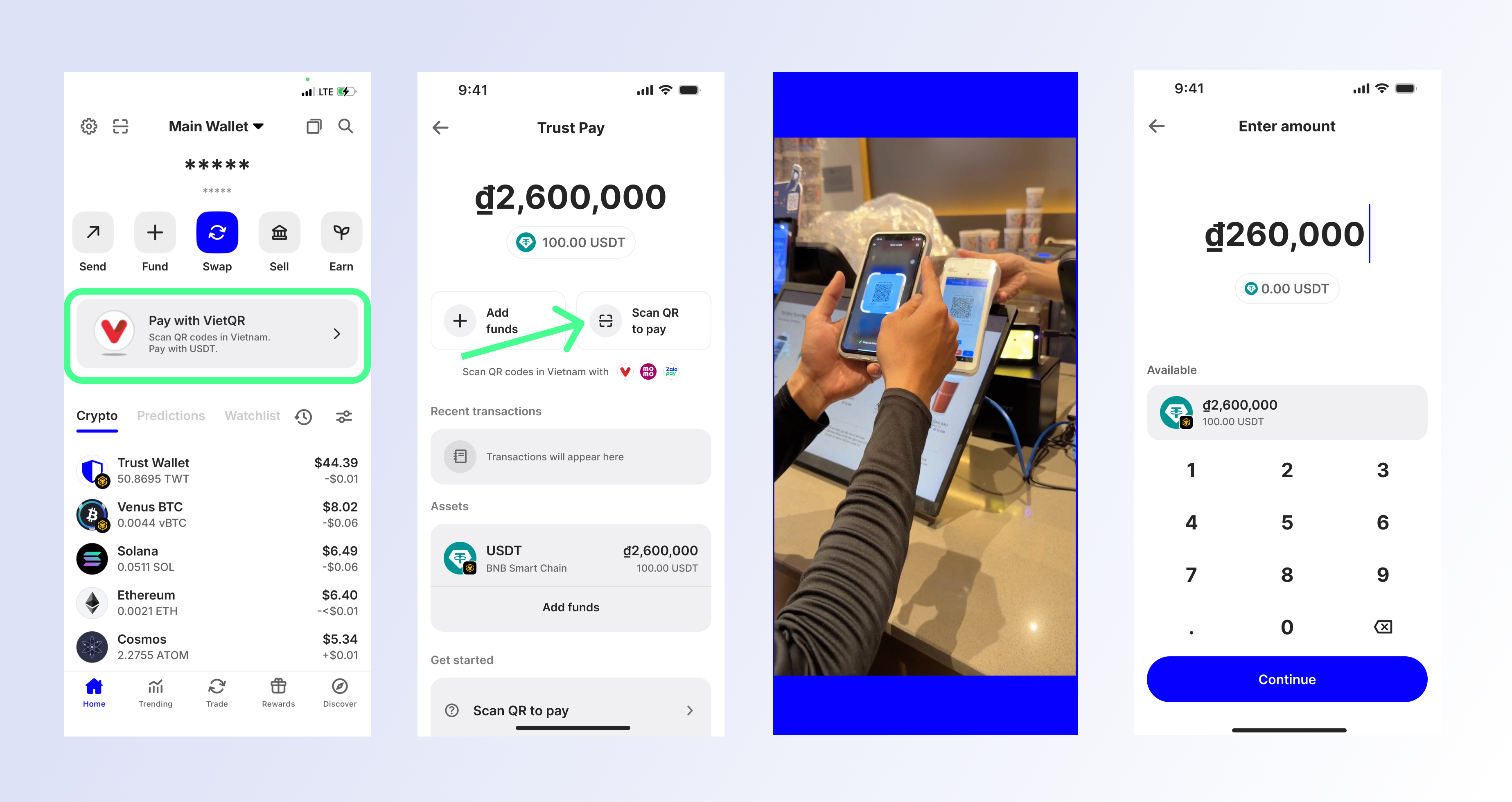

QR Codes Bridge Crypto and Offline Retail

QR codes function as the primary interface between on-chain stablecoins and physical point-of-sale systems. For merchants, this technology eliminates the need for specialized hardware upgrades, allowing existing card terminals to process USDC and USDT transactions through software integration. The user experience mirrors traditional NFC or card payments: the customer scans a static or dynamic code, confirms the transaction in their digital wallet, and receives immediate on-chain confirmation.

This workflow addresses the historical friction of cryptocurrency adoption by abstracting away complex wallet addresses and gas fee calculations. According to BVNK’s 2026 Utility Report, 30% of users cite lower fees as the primary driver for stablecoin adoption, while 28% prioritize security and 27% seek global access. By integrating stablecoins via QR, merchants can offer these benefits without requiring customers to navigate blockchain explorers or manage private keys manually.

The transition from card swipes to crypto checkout is not merely cosmetic; it fundamentally alters settlement finality. Traditional card networks require 1-3 days for funds to clear, during which time merchants face chargeback risks and interchange fees averaging 1.5-3.5%. Stablecoin QR payments settle on-chain in seconds, providing near-instant liquidity and eliminating chargeback fraud—a critical advantage for high-risk or digital goods merchants. Thunes notes that these trends are shaping global payments by enabling faster liquidity and enhanced compliance tracking for cross-border transactions.

Market data and price stability trends

Stablecoin payments rely on an asset class that must remain predictable. Unlike volatile cryptocurrencies, stablecoins are designed to maintain parity with fiat currencies, typically the US dollar. This stability is the foundation of their utility for merchant settlements, where finality and value preservation are non-negotiable.

The market demonstrates this reliability through consistent trading data. Major stablecoins like USDC and USDT trade in tight bands around their pegs, reflecting deep liquidity and arbitrage efficiency. For merchants, this means the risk of settlement value fluctuation during the transaction window is negligible.

To understand the depth of this stability, traders and analysts monitor the 24-hour price action of these assets. The following chart illustrates the recent trading behavior of USDC against the US dollar, highlighting the minimal deviation from the $1.00 peg.

This visual evidence supports the broader consensus among regulatory bodies and financial institutions. As noted in recent analyses by the Boston Consulting Group and the International Monetary Fund, the structural integrity of stablecoin markets is strengthening, driven by institutional adoption and clearer regulatory frameworks. For merchants, this trend signals a maturing infrastructure ready for high-volume, high-stakes settlement.

Stablecoin rails vs. traditional processors

For merchants, the choice between traditional card networks and stablecoin settlement rails comes down to two variables: cost structure and settlement finality. Traditional processors like Visa and Mastercard operate on a legacy model that introduces significant friction for cross-border and high-volume transactions. Stablecoins offer a direct alternative by leveraging blockchain infrastructure to bypass intermediary banking layers.

The economic advantage is measurable. Traditional card processing fees typically range from 1.5% to 3.5%, plus fixed per-transaction costs. In contrast, stablecoin transactions on efficient networks often cost less than 1% when accounting for gas fees and exchange spreads. This reduction is not merely theoretical; it directly impacts net revenue, particularly for low-margin goods or international sales where foreign exchange (FX) markups add further drag.

Settlement speed represents the second critical differentiator. Card networks operate on T+1 or T+2 settlement cycles, meaning funds are not immediately available for the merchant to use. Stablecoin payments settle in seconds or minutes, providing immediate liquidity. This speed reduces cash flow gaps and eliminates the need for reserve accounts that tie up working capital.

| Feature | Traditional Card Processors | Stablecoin QR Payments |

|---|---|---|

| Average Processing Fee | 1.5% – 3.5% + fixed fee | < 1% (network + exchange spread) |

| Settlement Time | T+1 to T+2 business days | Seconds to minutes |

| Chargeback Risk | High (reversible transactions) | Low (irreversible on-chain) |

| Cross-Border FX Cost | 2% – 4% markup | Near-zero (stable peg) |

The irreversibility of stablecoin transactions also removes the administrative burden of chargeback disputes. While this shifts some fraud responsibility to the merchant, it eliminates the hidden costs of dispute resolution and potential fund freezes. For businesses prioritizing efficiency and transparency, stablecoin rails provide a clearer, more predictable financial infrastructure than the opaque fee structures of traditional processors.

Steps to accept stablecoin payments today

Integrating stablecoin payments requires a structured approach to ensure regulatory compliance and operational stability. The process moves from provider selection to live deployment, prioritizing settlement finality and auditability.

Choose a processor that offers direct fiat settlement or compliant on-ramp services. Providers like Stripe and Thunes now support USDC and other major stablecoins, allowing merchants to receive fiat directly to their bank accounts. This avoids holding volatile crypto assets on your balance sheet and simplifies tax reporting. Verify that the provider maintains necessary Money Transmitter Licenses (MTLs) in your operating jurisdictions.

Set up dedicated payment addresses or dynamic QR codes for each transaction. Static addresses pose security risks and complicate accounting. Use a processor that generates unique payment identifiers for every invoice. This ensures that incoming transactions can be automatically matched to specific orders in your Point of Sale (POS) system, reducing manual reconciliation errors.

Before going live, execute test transactions using small amounts. Verify that the funds settle correctly in your processor’s dashboard and that the fiat conversion hits your bank account as expected. Check that your POS system correctly marks the order as paid. This step confirms that your integration handles network confirmations and provider API responses without delay.

Enable stablecoin payments for all eligible customers. Monitor the first few days of transactions closely to ensure settlement times align with your operational expectations. Most processors settle stablecoin payments in minutes, significantly faster than traditional ACH transfers. Keep logs of all transaction hashes for potential audit trails required by financial regulators.

No comments yet. Be the first to share your thoughts!