QR payments become the global rail

QR payments are no longer experimental. They are becoming the standard global rail for commerce, driven by stablecoins that settle in real time. This shift moves the industry away from slow batch processing toward instant finality.

The scale of this transition is massive. Juniper Research projects that QR code payments will exceed $8 trillion by 2029, representing a 50% growth from 2025 levels. In the United States alone, over 102 million people are expected to scan QR codes in 2026. These are not niche pilots; they are becoming part of daily operations for millions of consumers and merchants.

Stablecoins provide the underlying asset class for this growth. By pegging value to fiat currencies while leveraging blockchain infrastructure, they offer the speed of digital assets with the stability of traditional money. This combination eliminates the volatility risk that hindered earlier crypto-payment experiments.

The infrastructure is maturing rapidly. Merchants can now accept payments that settle instantly, reducing the need for complex reconciliation processes. As adoption increases, the network effects will make QR codes the default interface for cross-border and domestic transactions alike.

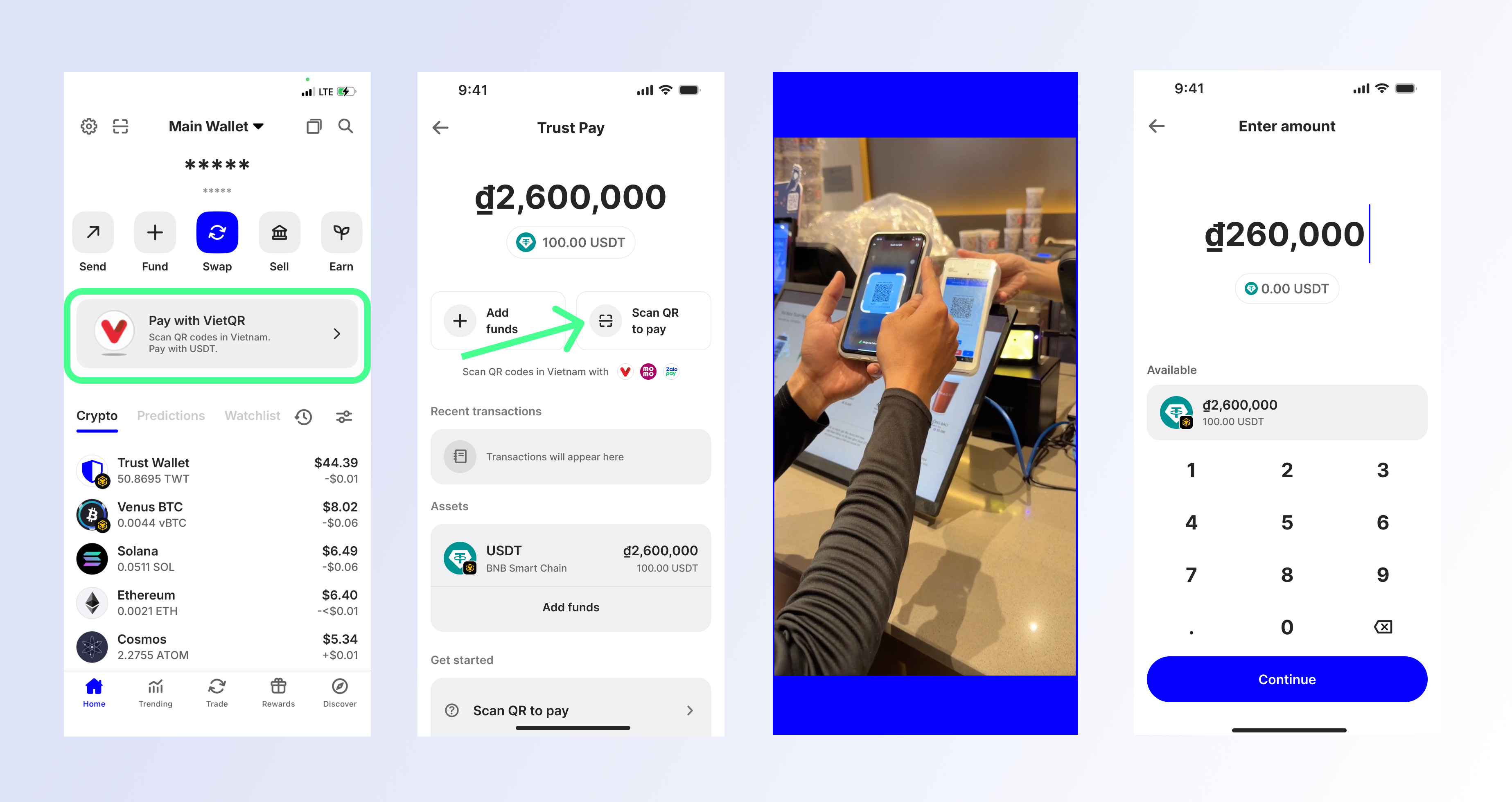

How stable QR pay works for merchants

Stable QR payments replace card networks with direct blockchain settlement. The merchant displays a static or dynamic QR code that encodes a wallet address and currency preference. When a customer scans the code, their wallet initiates a transfer of USDC or USDT. The transaction settles on-chain in seconds, bypassing the traditional card rails that typically take days to clear.

Unlike card payments, which involve multiple intermediaries and variable interchange fees, stable QR payments offer predictable costs and immediate finality. The merchant receives the stablecoin directly in their wallet, or a payment processor converts it to fiat instantly. This eliminates chargeback risk and reduces the time between sale and available capital.

The technical flow relies on the stability of the underlying asset. USDC and USDT are pegged to the US dollar, so merchants do not face the volatility risks associated with Bitcoin or Ethereum. A

demonstrates how tightly these assets track the dollar, providing the price stability merchants need for daily operations.

The merchant creates a QR code containing their wallet address and the desired currency (e.g., USDC). This can be a static code for small vendors or a dynamic code generated per transaction for higher security and automated reconciliation.

The customer opens their digital wallet app and scans the merchant's QR code. The app displays the transaction details, including the amount and currency. The customer reviews the information and confirms the payment.

The wallet broadcasts the transaction to the blockchain network. Miners or validators confirm the transfer of stablecoins from the customer to the merchant. This step typically takes a few seconds to a minute, depending on the network congestion.

The merchant's wallet receives the USDC or USDT. If using a fiat-on-ramp service, the stablecoin is automatically converted to the local currency and deposited into the merchant's bank account, often within minutes.

This direct settlement model reduces friction for both parties. Merchants avoid the 2-3% interchange fees associated with card payments, while customers enjoy faster checkout times. As QR code adoption grows, this infrastructure becomes a standard alternative to traditional payment methods.

Key stablecoin payment providers in 2026

The landscape of stablecoin payment providers has shifted significantly in early 2026. Major platforms are recalibrating their infrastructure to handle real-time settlements, with some exiting the space entirely while others double down on cross-border QR rails. This consolidation has left merchants with a clearer, albeit more specialized, set of options for accepting digital dollar payments.

Trust Wallet recently announced the temporary discontinuation of its native QR payments feature, effective March 31, 2026. The change stems from necessary updates to its underlying payment provider integration rather than a decline in demand. This move highlights the fragility of embedded crypto features within general-purpose wallets, where regulatory and operational shifts can abruptly alter service availability. Merchants relying on Trust Wallet for direct stablecoin settlement must now pivot to dedicated payment processors or alternative wallet solutions that offer more robust infrastructure partnerships.

Meanwhile, the focus has shifted toward specialized cross-border QR solutions. Markets like Vietnam are seeing explosive growth in this sector, with the State Bank of Vietnam reporting a 61.63% increase in QR payment transaction volume in the first nine months of 2025 alone. This trend is driving the development of new provider stacks that prioritize instant currency conversion and low-cost settlement, moving beyond simple peer-to-peer transfers to true merchant-grade infrastructure.

The following comparison table outlines the current capabilities of major stablecoin payment providers, focusing on settlement speed, supported assets, and geographic reach.

Advantages over traditional card networks

Stable QR payments remove the structural inefficiencies that define modern card processing. For merchants, the shift from legacy rails to blockchain-backed stablecoins changes the economics of every transaction. The benefits fall into three distinct categories: fee reduction, settlement speed, and global accessibility.

Lower fees without interchange

Traditional card networks operate as a toll bridge. Every swipe or tap triggers a cascade of fees: interchange fees paid to the card issuer, network fees for Visa or Mastercard, and processing fees for the merchant acquirer. These costs typically total 1.5% to 3.5% of the transaction value. Stable QR payments bypass this middleman layer entirely. Because the transaction settles on a blockchain using a stablecoin pegged to a fiat currency, there is no interchange fee to pay. Merchants pay only the minimal network gas fee, which is often a fraction of a cent. This margin preservation is critical for low-margin retail businesses.

Instant settlement vs. T+2 delays

Card networks operate on a T+2 settlement cycle. When a customer pays on Monday, the merchant often does not see the funds until Wednesday or Thursday. This delay creates cash flow friction and requires merchants to maintain larger working capital reserves to cover payroll and inventory during the gap. Stable QR payments settle in seconds. Once the customer scans the code and confirms the transaction, the stablecoin transfer is confirmed on the blockchain, and the funds are immediately available in the merchant’s digital wallet. This real-time liquidity allows businesses to reinvest capital faster and reduces the need for short-term bridging loans.

Global reach without currency friction

Cross-border card payments involve multiple currency conversions and correspondent banking fees. A merchant in the US accepting payment from a customer in Europe might see their funds converted to EUR, then back to USD, with each step incurring a spread and a fee. Stable QR payments eliminate this friction. Because the stablecoin remains pegged to a single currency (typically USD), the merchant receives the exact value of the sale regardless of the customer’s location. There is no currency conversion, no correspondent bank delays, and no hidden forex spreads. This makes stable QR payments a truly global payment rail, accessible to any merchant with a smartphone and an internet connection.

Implementation challenges for offline merchants

Transitioning to stablecoin QR payments introduces immediate operational friction for traditional retailers. The primary hurdle is not the adoption of digital currency itself, but the integration of legacy Point-of-Sale (POS) infrastructure. Most existing hardware lacks native support for the cryptographic verification required by blockchain settlements. Without specific software updates or hardware peripherals, merchants cannot generate or scan the unique QR codes necessary for real-time transaction initiation.

Customer education represents a secondary but significant barrier. Unlike credit card transactions, which rely on familiar magnetic stripe or NFC taps, stablecoin payments require consumers to navigate digital wallets and understand network fees. This friction can lead to abandoned carts if the checkout process feels cumbersome compared to traditional methods. Merchants must invest in clear signage and staff training to guide customers through the scanning and confirmation steps, ensuring the experience remains as frictionless as possible.

Regulatory compliance adds another layer of complexity, particularly for cross-border operations. Stablecoins operate on a global ledger, but payment regulations are strictly territorial. Merchants must navigate varying jurisdictional rules regarding anti-money laundering (AML) and know-your-customer (KYC) protocols. Failure to align with local financial authorities can result in frozen assets or legal penalties. For businesses operating in multiple regions, maintaining compliance across different regulatory frameworks requires robust internal controls and potentially localized payment processors.

The cost of these implementation challenges varies significantly by region and business size. Understanding the current market valuation of payment infrastructure providers can help merchants estimate their transition costs.

No comments yet. Be the first to share your thoughts!