What stable QR pay 2026 means for merchants

Stable QR pay 2026 combines the familiarity of scanning a code with the speed of blockchain settlement. When a customer scans a merchant’s QR code, the payment travels through a stablecoin network like USDC or USDT rather than the traditional card processor. The merchant receives funds in minutes, not days, and avoids the 2-3% interchange fees that eat into margins.

This system works across borders without the friction of currency conversion delays. A tourist from Europe can pay a vendor in Tokyo using their phone, and the merchant gets settled in local currency or their preferred stablecoin. The infrastructure relies on the fact that over 102 million Americans will scan QR codes in 2026, with QR-based payments expected to hit $3 trillion in annual spending. This volume makes the technology a standard, not a novelty.

For merchants, the shift is about control and cost. Traditional card rails require multiple intermediaries—acquirers, networks, and processors—each taking a cut. Stable QR payments cut out the middlemen. The transaction is peer-to-peer, secured by the blockchain, and settled directly into the merchant’s digital wallet. This reduces the risk of chargebacks and simplifies accounting for cross-border sales.

The technology is not just about speed; it is about accessibility. Small businesses that previously could not afford international payment gateways can now accept global customers with a simple printed QR code. No expensive POS hardware is needed. The code links directly to the payment contract, ensuring that the funds are available before the goods are handed over. This instant finality changes the risk profile for small retailers, turning high-risk international sales into low-friction transactions.

Setup your stable QR pay 2026 infrastructure

Accepting stablecoin payments requires a specific stack: a compatible wallet, a POS system that reads QR codes, and a payment provider that settles funds. Unlike credit card processing, stable QR pay 2026 workflows often bypass traditional banking rails, allowing for faster settlement and lower fees. However, the technical setup demands careful selection of providers, as the landscape shifts rapidly.

Follow these steps to configure your merchant infrastructure for stablecoin QR acceptance.

Start by selecting a provider that supports the stablecoins you want to accept (USDC, USDT, or DAI). Providers differ in supported networks (Ethereum, Polygon, Solana) and settlement options. Some offer instant fiat settlement to your bank account, while others allow you to hold crypto. Check their fee structures and API documentation before committing. Note that some major providers, like Trust Wallet, have adjusted their QR payment services recently, so verify current availability.

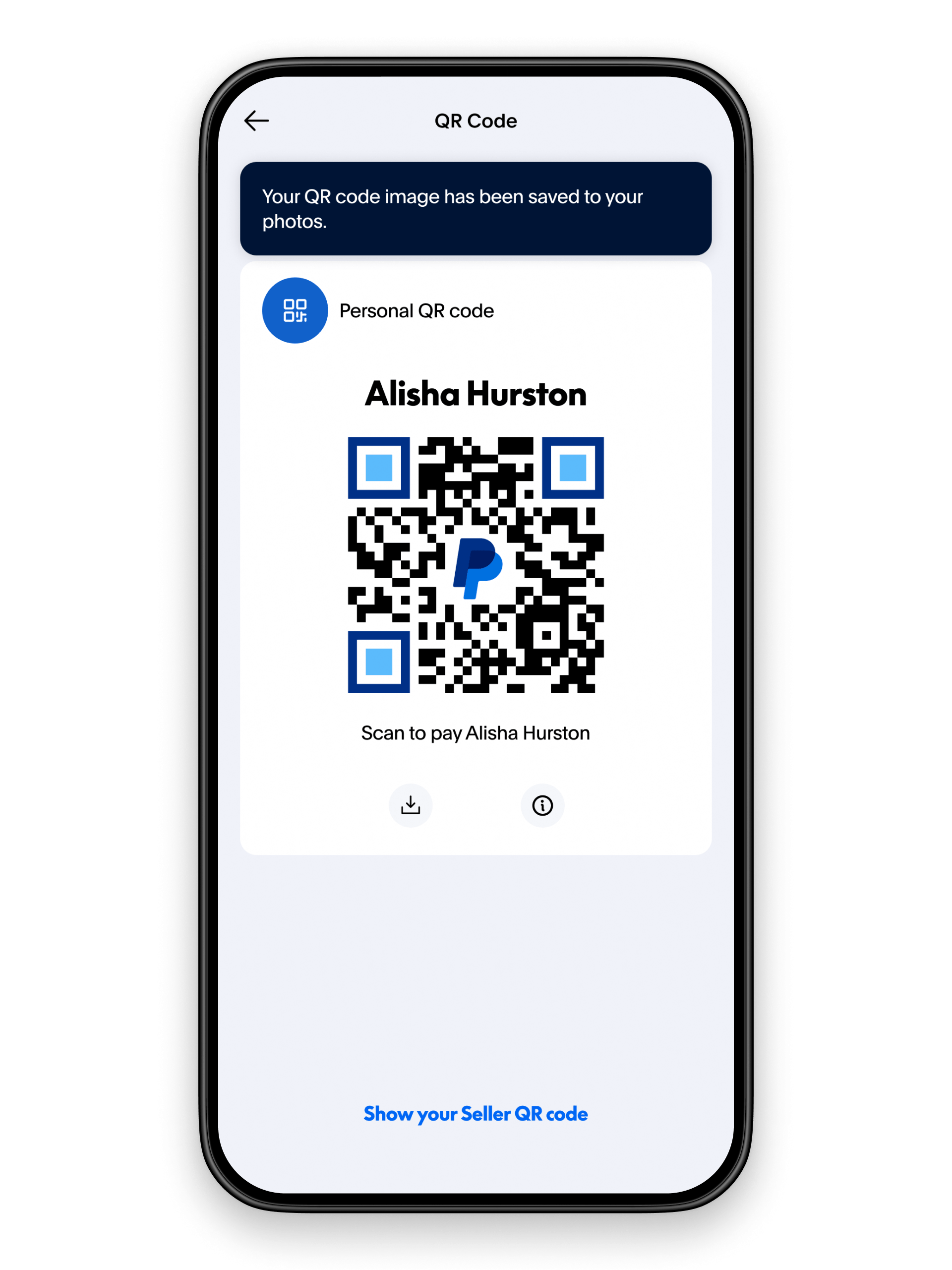

Create a dedicated merchant wallet for receiving payments. This wallet should be distinct from your personal treasury or cold storage. Ensure it is compatible with your chosen provider’s QR standard. Most providers require you to generate a unique merchant ID or QR code that links your wallet address to your business profile. Secure this wallet with multi-signature requirements if you are handling significant volume.

Your Point of Sale (POS) system must be able to generate and scan QR codes. If you are using a traditional POS, check if it supports crypto plugins or if you need a dedicated mobile app. For new setups, consider POS systems designed for digital payments that include built-in stablecoin support. The system should automatically generate a dynamic QR code for each transaction amount to prevent tampering.

Before going live, conduct end-to-end tests. Send small transactions from personal wallets to your merchant wallet via QR code. Verify that:

Test different networks (e.g., Polygon vs. Ethereum) to ensure compatibility across customer wallets.

Once tested, enable stablecoin payments for your customers. Display your QR code at checkout. Monitor transactions closely for the first few weeks to identify any integration issues or network congestion delays. Keep your provider’s API keys and wallet credentials secure and backed up.

How stable QR pay converts foreign currency

When a tourist scans a merchant's QR code, the interaction looks instant, but the backend handles a complex conversion chain. Unlike traditional card networks that route through multiple intermediaries, stable QR pay 2026 uses a streamlined path to settle funds in local fiat.

The process begins when the customer's wallet broadcasts a transaction in a stablecoin, typically pegged to the US dollar. The acquiring bank or payment processor receives this digital signal and immediately locks the exchange rate. Within seconds, the system converts the stablecoin value into the merchant's local currency. This happens before the final settlement occurs, protecting the merchant from volatility.

Traditional cross-border card payments often take 2-3 days to settle and incur fees of 2-4% due to foreign exchange markups and interchange fees. Stable QR pay 2026 reduces this timeline to seconds or minutes, with settlement fees often below 1%. The merchant receives the exact local currency amount in their bank account, eliminating the need for manual currency hedging.

Cost and speed comparison

The financial advantage becomes clear when comparing the mechanics of legacy systems against modern QR-based settlements. The table below highlights the differences in fees, speed, and cross-border capability.

| Feature | Traditional Card | Stable QR Pay 2026 |

|---|---|---|

| Settlement Time | 2-3 business days | Seconds to minutes |

| Cross-Border Fees | 2-4% + FX markup | 0.5-1% |

| FX Risk | Merchant bears risk | Locked at scan |

| Intermediaries | 4-5 parties | 2-3 parties |

Compliance and risk management in 2026

Stablecoin payments shift regulatory burden from the network to the merchant. Unlike traditional card networks that absorb chargebacks and fraud losses, accepting digital assets requires you to manage identity verification and transaction monitoring directly. The regulatory framework for stable QR pay 2026 is still solidifying, meaning your compliance stack must adapt to local laws rather than relying on a single global standard.

Managing AML and KYC obligations

Anti-Money Laundering (AML) and Know Your Customer (KYC) requirements vary significantly by jurisdiction. In many regions, merchants exceeding certain transaction thresholds must register as virtual asset service providers (VASPs). This often involves integrating third-party identity verification tools that screen customer wallets against sanctions lists before settlement. Failure to implement these checks can result in frozen funds or heavy fines, regardless of your intent.

Mitigating volatility with stablecoins

The primary risk in crypto payments is price fluctuation. Stablecoins pegged to fiat currencies like the US dollar eliminate this exposure, but they do not remove regulatory scrutiny. You must ensure your payment processor supports real-time conversion to fiat or holds sufficient stablecoin reserves to cover settlements. This mechanical hedge protects your margins while keeping your business compliant with financial stability regulations.

Tax reporting and record-keeping

Tax authorities treat cryptocurrency transactions as property in many jurisdictions. Every stablecoin payment triggers a taxable event that must be recorded with a timestamp, value, and counterparty information. Maintain detailed logs of all incoming and outgoing transactions to simplify year-end reporting. Automated accounting software that integrates with your payment gateway can reduce manual errors and ensure you meet audit requirements.

Common questions about stable QR pay 2026

Checklist for launching stable QR pay 2026

Before going live, verify your technical stack supports the stablecoin standards you intend to use. Confirm your POS system can handle the specific QR formats (EMVCo or proprietary) required by your target markets, and ensure your treasury wallet has sufficient liquidity for instant settlement.

Legal compliance is non-negotiable for cross-border operations. Register as a money services business if required in your jurisdiction, and implement AML/KYC checks that align with the stablecoin issuer’s terms. Review tax reporting obligations for cryptocurrency transactions to avoid penalties.

Operational readiness ensures a smooth customer experience. Train staff on troubleshooting failed scans and refund procedures. Set up monitoring alerts for transaction anomalies, and test the full payment flow with small amounts in both testnet and production environments before opening your doors.

No comments yet. Be the first to share your thoughts!