Stable QR pay 2026: The FX Fee Solution

Stable QR pay 2026 marks a shift from speculative crypto experiments to practical cross-border utility. By anchoring payments to stablecoins, merchants and travelers bypass the 3-5% foreign exchange fees that traditional card networks charge. This isn't just about lower costs; it's about speed and transparency in an era where global commerce moves instantly.

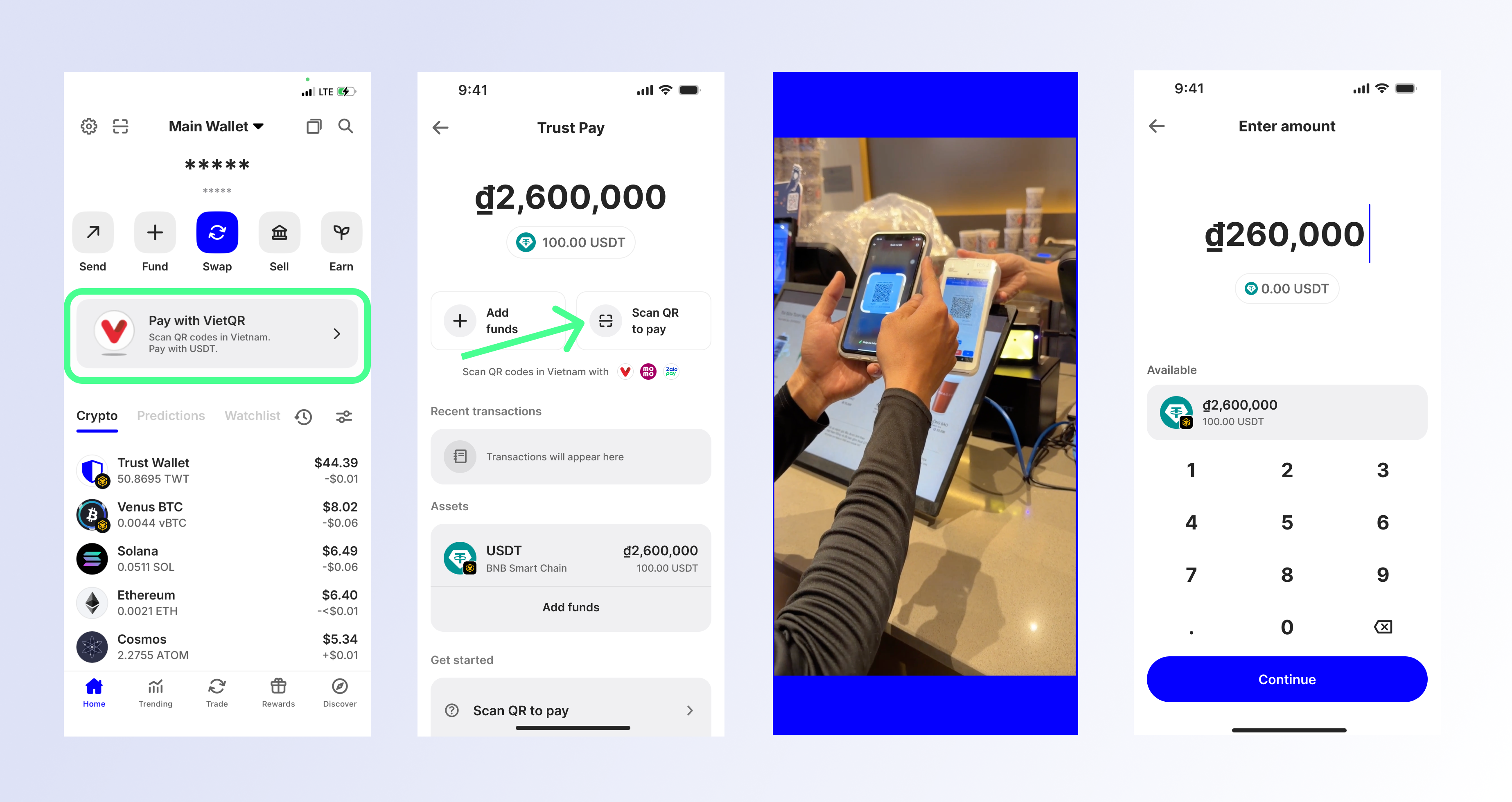

The infrastructure is already live. As of April 2026, Chinese tourists can scan VIETQRGlobal codes via Alipay to pay at Vietnamese shops, restaurants, and hotels. This pilot program demonstrates how stablecoin rails can integrate with existing QR standards, effectively creating a borderless payment layer without requiring new hardware for small businesses. The QR code market itself is expanding, with values projected to exceed $8 trillion by 2029, driven largely by this seamless cross-border integration.

However, the technology isn't without its trade-offs. While QR codes are more relevant than ever—used by over 100 million Americans in 2026—the security burden shifts to the processing platform rather than the code itself. Users must trust the underlying wallet and the stablecoin issuer. For businesses, the advantage is clear: instant settlement and eliminated FX friction. For consumers, the risk lies in understanding which wallets and codes are officially supported in their destination.

The future of cross-border payments lies in this hybrid model: familiar QR scanning technology backed by stablecoin settlement. As more international financial centers pilot these systems, the friction of currency conversion will likely vanish for the average traveler.

Stable qr pay 2026 choices that change the plan

Stable QR payments eliminate traditional foreign exchange (FX) spreads, but they introduce different operational variables. Before integrating this system, merchants must weigh speed against cost and convenience against security. The following comparison breaks down the concrete factors that determine whether this model fits your transaction volume and risk profile.

| Factor | Stable QR Pay | Traditional FX Card | Direct Crypto Wallet |

|---|---|---|---|

| FX Fees | Near-zero (pegged to USD/EUR) | 1.5%–3% foreign transaction fee | Network gas fees (volatile) |

| Settlement Speed | Seconds to minutes | 1–3 business days | Minutes (blocker dependent) |

| Price Volatility | Low (stablecoin peg) | None (fiat settlement) | High (asset price swings) |

| Merchant Adoption | Growing in APAC/EMEA | Global (universal) | Niche (tech-savvy only) |

| Security Model | App-dependent (phishing risk) | Card network fraud protection | Irreversible transactions |

The primary advantage is cost efficiency. Traditional cross-border payments often bleed value through multiple intermediary banks and dynamic currency conversion fees. Stable QR systems bypass this chain, settling directly in a pegged asset like USDC or USDT. For high-volume merchants, this margin preservation is significant. However, this benefit assumes the stablecoin maintains its peg. Any de-pegging event during the settlement window can erase these savings instantly.

Speed is the second major factor. While traditional cards take days to clear, stable QR transactions settle on-chain almost immediately. This liquidity improves cash flow for businesses that rely on daily turnover. Yet, this speed comes with a tradeoff: the lack of chargeback protection. If a customer disputes a transaction, the funds are already gone. Merchants must implement their own dispute resolution mechanisms or rely on platform-specific protections, which vary widely by region.

Finally, consider the user experience. QR codes are increasingly standard, with over 100 million Americans expected to use smartphone QR scanners in 2026. This familiarity reduces friction for consumers. However, security risks remain. Unlike NFC or card networks, QR codes themselves do not encrypt the transaction data; the app or platform processing the transaction handles security. Users must be vigilant against "quishing" (QR phishing), where malicious codes redirect payments to fraudulent accounts. Merchants should educate customers on verifying merchant codes to mitigate this risk.

How to choose a stable QR pay provider

Cross-border transactions often fail because of fragmented infrastructure. A merchant in Vietnam cannot simply accept a payment from a tourist in China without a bridge. You need a provider that connects multiple national QR standards through a single integration. This guide walks you through the technical and operational checks required to select the right stable QR pay partner.

Most national QR systems (like India’s UPI or Thailand’s PromptPay) are domestic. Your provider must support cross-border linking protocols, such as the ASEAN Cross Border QR or China’s VIETQRGlobal standard. Without this, you are limited to local transactions only. Check if the provider has active connections to the specific countries you plan to serve. If they only support one-way flows, they will not work for a global merchant.

Stable QR payments rely on instant conversion. When a customer scans a code, the underlying stablecoin must be swapped for local fiat for the merchant, or vice versa. Ask the provider about their liquidity pools. Do they hold reserves in the destination currency? If not, your settlement times will suffer, and exchange rate fluctuations will eat into your margins. Prioritize providers with deep, real-time liquidity in both the origin and destination currencies.

Cross-border payments trigger strict anti-money laundering (AML) and know-your-customer (KYC) rules. A provider operating in multiple jurisdictions must hold the necessary licenses in each. Look for partnerships with regulated payment service providers (PSPs) rather than relying on unregulated crypto exchanges. If the provider cannot produce a clear compliance map for your target markets, walk away. The risk of frozen funds is too high for business continuity.

The best technology is useless if your point-of-sale (POS) system cannot talk to it. Evaluate the provider’s API documentation and SDK availability. Do they offer pre-built plugins for major e-commerce platforms like Shopify or WooCommerce? For physical retail, does the provider support standard QR scanning hardware? A complex integration that requires custom development for every new feature will slow your rollout and increase technical debt.

FX fees are not just the spread. They include conversion fees, cross-border transfer fees, and potential withdrawal fees. Request a full fee schedule for a typical transaction. Compare the all-in cost against traditional methods like PayPal or Wise. If the savings are less than 2-3%, the operational complexity of managing stablecoin wallets may not be worth it. Aim for providers that offer transparent, flat-rate pricing without hidden FX markups.

Before committing to a full rollout, test the system with small, real-world transactions. Send and receive payments across the intended borders. Monitor settlement times, failure rates, and customer support responsiveness. This is the only way to verify that the theoretical interoperability works in practice. If the pilot reveals delays or errors, you can negotiate fixes or switch providers before scaling up.

Spotting Weak Options and Misleading Claims

Not every QR payment solution eliminates FX fees. Some providers use the label "zero fees" while quietly applying dynamic currency conversion (DCC) markups at the point of sale. DCC locks in an unfavorable exchange rate the moment the transaction begins, often costing the user 3-5% more than the true wholesale rate.

To avoid this, check if the QR code is linked to a local clearing network like Thailand’s PromptPay or Vietnam’s VietQR. These systems settle in local currency and bypass the international card networks that typically charge 2-3% in cross-border fees. If the merchant’s terminal asks you to choose between paying in your home currency or the local currency, always pick the local option. Choosing your home currency triggers DCC.

Another trap is the "flat fee" model. While it sounds simpler than percentage-based fees, a fixed $0.50 or €0.30 charge per transaction can be disproportionately expensive for small purchases. For a $5 coffee, a flat fee represents a 10% cost, which is far worse than a 0.5% FX spread. Calculate the break-even point: if the flat fee exceeds your expected FX spread on typical transaction sizes, the model is likely more expensive than it appears.

Stable qr pay 2026: what to check next

Stable QR pay removes the friction of currency conversion, but it introduces new operational considerations. Before adopting this infrastructure, merchants and travelers should understand the practical tradeoffs between speed, cost, and security.

No comments yet. Be the first to share your thoughts!